-

Whatsapp

+1 689 248 1956 -

Email

joannewong0817@gmail.com

21/05/2026

21/05/2026

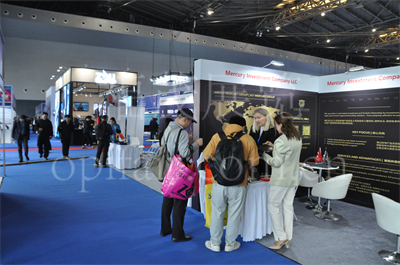

In the investment process, many people focus on returns, but what truly influences the stability of long-term decisions is often the level of understanding of risk. Different investment projects differ in their funding cycles, market volatility, and return structures. Without a systematic understanding, it’s easy to make unreasonable judgments due to insufficient information. Investment expos bring together a variety of investment projects and industry resources, allowing visitors to compare projects and engage in on-site discussions. This allows for a more intuitive understanding of the risk characteristics of different investment models, thereby improving overall risk awareness. Multiple Project Displays Help Identify Risk Differences Different investment models are presented together. Investment expos typically cover real estate, finance, and industrial projects, each with distinct risk characteristics. Visitors can directly observe the differences in project cycles, returns, and stability. Multi-dimensional displays make risk understanding more intuitive. On-site Interaction Enhances the Depth of Risk Understanding Face-to-face communication makes information more concrete. Project representatives or advisors explain potential market changes and financial pressures during the investment process, reducing the risk of one-sided understanding. Consultations further clarify the sources of risk and coping strategies. This exchange enhances risk assessment capabilities, making on-site interaction a more comprehensive understanding. Multidimensional analysis helps build rational judgment Horizontal analysis enhances decision-making awareness. Different projects differ significantly in return models and risk levels:comparison makes it easier to understand the balance. Selection based on individual needs: Investors can choose suitable directions based on their budget and risk tolerance. Rational analysis makes investment decisions more robust. In the overall experience of the investment expo, risk awareness is not an abstract concept, but rather a clear understanding gradually formed through project demonstrations, case studies, and on-site discussions. Visitors can quickly encounter different investment models and understand the relationship between risk and return…

20/05/2026

20/05/2026

In an ever-changing investment market, more and more people are realizing that a single investment approach is insufficient for long-term asset planning. Different investment models differ significantly in terms of risk, return, timeframe, and capital requirements. A lack of systematic understanding can easily lead to missing out on suitable opportunities due to limited information. Investment expos bring together various types of investment projects, allowing visitors to understand the characteristics and logic of different investment models in a unified setting, thus gaining a more comprehensive understanding of the market structure. Multi-industry Project Showcase Broadens Investment Horizons Diverse investment models are presented in a concentrated manner. Investment expos typically cover multiple areas, including real estate, finance, industry, and cross-border investment. Visitors can directly observe the differences in the operational methods of different models. Diverse information broadens investment horizons. On-site Interaction Enhances Investment Understanding Face-to-face communication makes information more concrete. Project representatives or consultants will introduce the return structures and participation methods of different investment models. Reduces vague understanding of investment concepts. Consultations provide a clearer understanding of the characteristics of various models and their suitable target groups. This exchange improves learning efficiency. On-site interaction deepens investment understanding. Multidimensional comparisons aid in investment judgment Horizontal analysis makes differences more apparent. Different investment models differ in risk levels, return cycles, and capital requirements; the comparison process strengthens judgment. Simultaneously, investors can select more suitable directions based on their own needs. This approach optimizes investment strategies, and reasonable comparisons make investment choices clearer. In the overall experience of the investment expo, diverse investment models are no longer just abstract concepts, but are gradually understood through project demonstrations, on-site explanations, and comparative analysis. Visitors can quickly grasp different investment logics and understand the differences and connections between various models. This centralized information acquisition method…

09/05/2026

09/05/2026

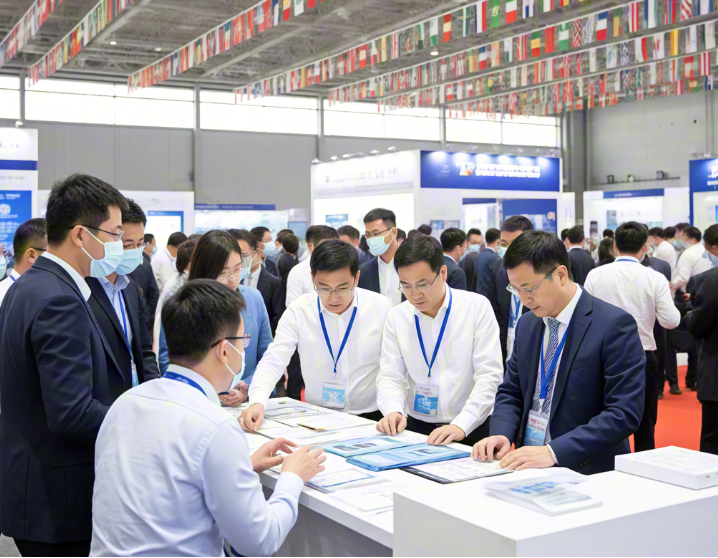

During the investment decision-making process, many individuals encounter the dual challenge of information overload coupled with a lack of professional judgment—a predicament particularly acute when navigating diverse asset classes and complex return structures, where relying solely on personal experience often proves insufficient for making sound choices. An investment expo serves as more than just a platform for the centralized display of projects; it also brings together industry experts, investment advisors, and project developers for on-site interaction, thereby offering visitors the opportunity to obtain professional advice directly and, in turn, enhance the overall quality of their investment assessments. On-Site Experts Provide Professional Investment Insights Face-to-face interaction deepens informational understanding. Investment expos typically invite industry analysts or investment advisors to provide detailed explanations regarding the market logic underpinning various projects. To facilitate the comprehension of complex investment structures, these experts elucidate sources of return, key risk factors, and prevailing market trends, making it easier for investors to grasp the fundamental essence of each project. This approach significantly elevates the level of professional insight available to attendees. Targeted Consultation Enhances Decision-Making Accuracy Personalized inquiries receive direct, specific answers. Visitors are empowered to pose questions to experts tailored to their own specific capital resources and risk tolerance. Experts respond by offering advice grounded in these practical circumstances, assisting investors in determining whether a particular project aligns with their individual needs and is suitable for investment. This form of dialogue substantially enhances the practical value of the information used to inform investment decisions. Multi-Project Analysis Combined with Professional Advice Offers a More Comprehensive Perspective Comparative analysis refines the quality of judgment. Within the confines of a single expo, visitors can simultaneously explore multiple investment opportunities and evaluate them in light of expert opinions. This process streamlines the investment selection journey, as professional guidance…

08/05/2026

08/05/2026

For those new to investing, the biggest challenge is often not choosing projects, but rather not knowing where to begin. The market is flooded with investment information, with significant differences between industries and business models. Without basic knowledge, it’s easy to make incorrect judgments due to information overload. Investment expos bring together multiple industries and investment projects of different types, allowing beginners to understand market structure and investment logic in a unified setting. Through on-site interactions and project comparisons, many previously abstract investment concepts become more intuitive. Therefore, these expos offer valuable introductory resources for investment novices. Concentrated Display Helps Build Basic Knowledge Multiple investment directions presented simultaneously. Investment expos typically cover real estate, finance, and industrial projects, allowing beginners to experience different investment types at once. Reduces the problem of fragmented information: Observing multiple projects in the same environment helps in understanding the basic investment structure. This approach helps build initial knowledge. On-site Interaction Reduces the Difficulty of Understanding Face-to-face communication makes information absorption easier. Project representatives or advisors will explain the project model, revenue sources, and basic risks. Interactive sessions ensure timely answers to questions. Beginners can directly ask questions, improving comprehension efficiency. This exchange enhances the learning experience. Comparing Multiple Projects Cultivates Judgment Skills Horizontal analysis makes differences more apparent. Different projects vary in risk, cycle, and return; comparison makes it easier to identify key characteristics. Simultaneously, the analytical process enhances judgment awareness, allowing beginners to gradually understand which types of investments best suit their funds and goals, thus optimizing their investment approach. Throughout the investment expo experience, novice investors can gradually build basic knowledge in a centralized information environment, rather than simply learning about a single project. Multi-industry displays, on-site interactions, and comparisons between different investment models make the originally complex market structure…

06/05/2026

06/05/2026

With the increasing abundance of investment channels available today, investors of all sizes are looking for suitable ways to participate. Small investors, in particular, are concerned about obtaining effective information and opportunities within a limited budget. Investment expos bring together investment projects from multiple industries and of varying sizes, allowing visitors to understand different investment thresholds and participation methods in a single setting, thus determining whether participation is suitable for them. Diversified Projects Lower the Barrier to Entry Projects of different sizes are showcased together. Investment expos typically cover real estate, finance, and asset-light projects, some of which have lower entry barriers. Small investors can filter for suitable project types based on their financial situation. This structure increases the likelihood of participation. Transparent On-Site Information Facilitates Rational Judgment Public explanations reduce information errors. Exhibit projects usually explain their funding structure, profit model, and basic risks, making them easier for small investors to understand. On-site explanations also allow for a more intuitive assessment of whether the project aligns with their risk tolerance. This approach enhances decision-making security. Comparative Environments Help Control Investment Risk Multiple projects on-site facilitate horizontal analysis. The concentrated display of different investment projects at expos helps in comparing differences in returns and risks. Smaller investors can compare and choose more stable investment opportunities. This approach optimizes the quality of their choices. Throughout the investment expo experience, smaller investors are not at an informational disadvantage; on the contrary, they can gain clearer judgment criteria through centralized displays and on-site exchanges. Diverse projects and transparent explanations enable participants with smaller capital to find options suitable for their risk tolerance, thereby enhancing the rationality and security of their investment decisions.

27/04/2026

27/04/2026

With increasingly diversified investment options and more complex information sources, many people tend to focus on only partial information when faced with different projects, lacking the ability to make overall judgments. Investment expos, by showcasing multiple industries and different types of investment projects in a unified setting, integrate information previously scattered across various platforms, allowing visitors to quickly build a basic cognitive framework. Furthermore, these events provide project demonstrations and, through on-site exchanges and comparative analysis, allow investors to more intuitively understand market structures, thus contributing to improved investment awareness. Concentrated Information Display for More Systematic Understanding Presenting multiple projects simultaneously enhances overall understanding. Investment expos typically cover real estate, finance, and various other industry investment projects, exposing visitors to different investment types. Reduces the Impact of Fragmented Information on Judgment: Comparing different project structures in a unified environment helps build a basic investment framework. This approach leads to more complete understanding. On-site Exchanges Enhance the Depth of Investment Understanding Communication ensures information goes beyond the surface. Project representatives or advisors explain the sources of returns, risk structures, and operational logic. Interactive learning enhances information absorption efficiency Asking questions allows for a deeper understanding of specific investment details, reducing misunderstandings. This exchange deepens cognitive understanding. Multidimensional Comparative Optimization of Investment Judgment Capability Horizontal comparison clarifies differences. Different projects are presented simultaneously in terms of returns, cycles, and risks, facilitating comparative analysis. The analysis process improves judgment:combining one’s own capital and risk appetite to select projects helps in forming rational decisions. This approach optimizes investment decisions. In the environment of an investment expo, information acquisition is no longer fragmented reception but rather a systematic understanding formed through centralized displays and interactive exchanges. Visitors can encounter multiple investment logics in a short time and gradually understand market differences through…

24/04/2026

24/04/2026

In the investment process, policy factors often directly impact project feasibility and future returns. However, relevant policy content is usually scattered and technically presented, making it easy for ordinary investors to misunderstand when researching on their own. Investment exhibitions, by showcasing different projects and industry information in a centralized manner, coupled with on-site explanations and consultations, provide visitors with opportunities to understand the policy background. In the same setting, the policy environments involved in different projects are systematically presented, allowing visitors to further understand their actual impact through interaction. This approach helps transform abstract policy content into more easily understood information, thereby improving overall judgment. Centralized Display Makes Policy Information More Accessible The gathering of multiple projects brings diverse policy content. Investment exhibitions typically cover multiple industries and fields, with each project involving corresponding policy background explanations. Simultaneously, centralized information reduces the difficulty of searching; visitors can encounter different policy content in the same setting without having to search separately. This method improves information acquisition efficiency. On-site Explanations Help Understand Policy Meaning Professional explanations make the content clearer. Project representatives or relevant personnel will explain the policy environment, helping to understand its impact on investment. The interaction process enhances understanding: Asking questions allows for a deeper understanding of policy details and scope of application, avoiding misunderstandings. This interaction makes policy information more concrete. Multiple comparisons improve judgment accuracy Different policy environments create a comparative framework. At the exhibition, policy differences between different projects or regions can be compared to determine their respective advantages. Combining policy conditions with investment objectives allows for a more rational assessment of project value. This approach makes decision-making more robust. In the environment of investment exhibitions, policy information is no longer fragmented and difficult to understand, but gradually becomes clear through display and…

22/04/2026

22/04/2026

In the investment decision-making process, project risk assessment is a crucial step influencing the final choice. However, much risk information is often hidden within the complex project structure and market background, making it difficult to grasp comprehensively through a single channel. Investment exhibitions, by showcasing multiple projects in a concentrated setting and providing opportunities for on-site exchange and comparison, allow visitors to access a wealth of information in a unified environment. Combined with direct communication with project teams and multi-dimensional comparisons, this offline setting helps to present risk factors more concretely, thereby improving the clarity of judgment and providing investors with a more complete reference basis before making a decision. Concentrated Display Makes Risk Information More Transparent Presenting multiple projects side-by-side facilitates the observation of differences. Investment exhibitions typically showcase project background, financial structure, and operating models, giving visitors a preliminary understanding of the basic situation. Concentrated Information Reduces Missed Risk Points: Comparing multiple projects in the same setting makes it easier to identify potential differences and inconsistencies. This approach helps in the initial identification of risks. On-site Communication Supplements Key Risk Details Face-to-face communication enhances the depth of information. Visitors can ask project teams or advisors about investment cycles, return stability, and potential uncertainties. Asking questions about key issues allows for a deeper understanding of project risk control measures and response plans. This communication method improves information reliability. Multi-dimensional comparison enhances risk assessment capabilities Horizontal comparison makes the risk structure clearer. Different projects presented at the same exhibition allow for comparison in terms of profit models, capital security, and industry background. Analyzing differences improves judgment accuracy: Screening based on one’s own risk tolerance helps avoid high-risk or mismatched projects. This approach optimizes overall decision-making. In the environment of investment exhibitions, risk information is no longer scattered…

18/04/2026

18/04/2026

In a constantly changing investment environment, emerging industries often represent new growth opportunities. However, this information is usually scattered across different channels, making it difficult for ordinary investors to quickly and systematically capture trends. Investment Expo, by showcasing projects and companies from multiple sectors, present industries at different stages of development in a unified space, allowing visitors to observe market trends. Through on-site exchanges and information comparison, visitors can understand mature industries and gain easier access to growing emerging sectors, thereby improving their ability to judge future investment directions. Multi-Sector Showcases Present New Industry Trends Concentrated displays make emerging directions more intuitive. Investment Expotypically cover multiple sectors such as technology, energy, and finance, including many rapidly developing emerging industry projects. Concentrated information facilitates overall observation: Visitors can quickly identify which industries are in the growth stage through side-by-side comparisons. This approach helps capture market changes. Project Exchanges Provide Industry Development Information Communication makes trend judgments more concrete. Through exchanges with company representatives, visitors can understand the industry’s development background, technological advancements, and market prospects. Asking questions specific to a particular industry helps assess its development potential and risk structure. This approach improves the accuracy of understanding. Horizontal comparison helps identify potential industries Comparing multiple projects highlights differences. Simultaneous presentation of projects from different industries at the exhibition helps observe growth rates and resource investment. Combining market demand and development cycles makes it easier to screen for promising emerging industries. This approach optimizes investment direction. In the environment of investment Expo, emerging industries are no longer scattered information points, but gradually become clearer through concentrated displays and in-depth exchanges. Visitors can access development dynamics from multiple fields in a short time and form more comprehensive judgments through comparison and communication. This approach improves information acquisition efficiency, helps identify…

16/04/2026

16/04/2026

When making investment decisions, a project’s profit structure is often a crucial factor in determining its value. However, much information presented online is often generalized and lacks detailed support, making it difficult to fully understand. Investment Expo, by showcasing multiple projects and combining on-site explanations and interactive consultations, provide visitors with a more intuitive way to obtain profit information. In this environment, the sources, distribution methods, and influencing factors of different investment projects’ profits can be presented more clearly, making the originally abstract profit model more concrete, thus helping investors make more rational judgments and comparisons. On-site demonstrations make profit information more intuitive and clear Concentrated explanations make the structure easier to understand. At investment Expo, project teams typically demonstrate their profit sources and basic structure through materials, demonstrations, or explanations. Visitors can compare the profit models of different projects in the same setting, quickly establishing an initial understanding. This method makes the profit structure more visual. Face-to-face communication supplements detailed information Exchange makes the profit logic more complete. Visitors can directly ask project teams about key information such as the profit cycle, risk factors, and distribution rules. For complex revenue structures, on-site explanations can further clarify their operational logic. This interaction enhances the credibility of information. Multiple project comparisons improve judgment accuracy Horizontal comparisons make differences more apparent. Displaying different projects in the same setting facilitates observation of the differences and characteristics between revenue structures. By comprehensively analyzing revenue levels and risk factors, project value can be judged more rationally. This approach improves overall decision-making efficiency. In the context of investment Expo, revenue structures are no longer abstract concepts but are gradually clarified through demonstrations and communication. Visitors can understand the revenue models of multiple projects in a short time and deepen their understanding through comparison and…

Number

NumberCall Now:

139 1723 4508

WeChat

WeChat

Form

FormBook Your Booth

Complete your information immediately and provide you with exclusive services!

Back to Top