-

Whatsapp

+1 689 248 1956 -

Email

joannewong0817@gmail.com

13/03/2026

13/03/2026

Investment immigration has increasingly become a popular strategy for high-net-worth individuals and families seeking international residency planning. Through investment immigration, applicants can not only obtain overseas residency or even citizenship but also gain more options in education, healthcare, lifestyle, and wealth management. With globalization and the growing mobility of talent, investment immigration is gradually viewed as an important means to improve quality of life and optimize family planning. Many families attend investment expos to learn about different countries’ investment immigration programs and obtain the latest policy information, helping them make more informed and strategic decisions. Obtaining international residency and citizenship One of the core advantages of investment immigration is that it provides legal overseas residency, and in some countries, applicants may directly obtain citizenship. With the status granted, family members can enjoy flexible living and travel arrangements, which is particularly valuable for those seeking a transnational lifestyle. Flexible living arrangements: Applicants can choose to reside long-term, short-term, or travel frequently in the host country, enjoying a high degree of mobility. Coverage for family members: Most investment immigration programs allow spouses and children to apply together, enabling access to education, healthcare, and social benefits. Travel convenience: Holding the host country’s status often provides visa-free access or simplified visa procedures, making international travel for business, leisure, or work easier. Life security: Choosing to live in a country with stable political and economic conditions helps safeguard family well-being and property, reducing uncertainties. Through investment immigration, families can enhance international mobility and create broader opportunities for children’s education and career development. Educational and lifestyle advantages Investment immigration provides significant benefits for family life and children’s education, which is a key reason many families pursue this route. Access to quality education: Children can attend local schools, international schools, or universities, benefiting from high-quality educational…

09/03/2026

09/03/2026

With the development of globalization, more and more families are paying attention to investment immigration and hope to obtain overseas residency or citizenship through financial investment. Investment immigration is not only related to identity planning but also involves asset allocation and long-term family development. Therefore, “how much money is required for investment immigration” has become one of the most common questions for people exploring such programs. Requirements vary widely between countries, and the total budget depends on investment thresholds, investment methods, and additional related costs. Investment thresholds vary by country Countries offer different investment immigration programs in order to attract international capital and talent, so the required investment amounts can differ significantly. Some countries set relatively low investment thresholds to attract international investors, with requirements starting at around $100,000 to $200,000. In several European countries, investment immigration programs are often linked to real estate purchases, with investment levels typically ranging from $250,000 to $500,000. In certain developed economies where demand is high, the investment requirement may exceed $500,000. Some programs require investors to maintain the investment for several years before they become eligible to apply for permanent residency or citizenship. Different investment options require different capital amounts Investment immigration programs usually offer several investment pathways, and the required capital depends on the type of investment chosen. Real estate investment: Purchasing property in the destination country is one of the most common options. Business investment: Establishing or investing in a local company to support economic development while meeting immigration requirements. Government funds or donations: Some programs allow applicants to contribute to government development funds. Financial investments: In certain countries, applicants may invest in government bonds or approved financial products. When choosing an investment option, it is important to evaluate factors such as financial security, investment duration, and potential returns. …

28/02/2026

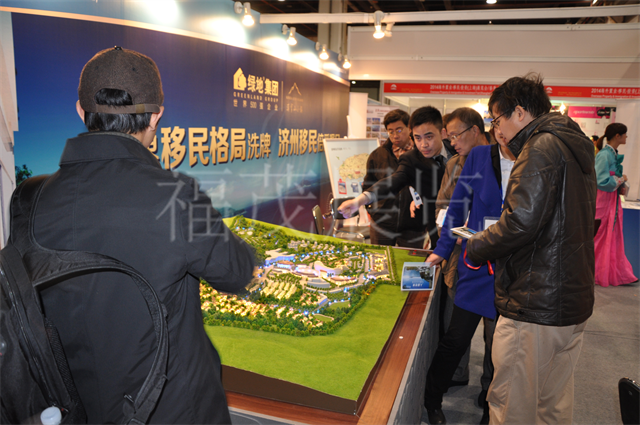

Against the backdrop of a deepening global trend towards diversified asset allocation, overseas real estate has gradually become an important focus for investors. Whether for risk diversification, asset structure optimization, or paving the way for future family life and education planning, cross-border property investment carries a longer-term significance. However, different countries have significant differences in economic environment, legal system, tax system, and market cycle. Without a systematic understanding and prior preparation, investment risks may be underestimated. What should you pay attention to when investing in overseas real estate? A comprehensive understanding of key factors before making a move is an important foundation for achieving stable returns. Market Environment and Development Potential Assessment The value of overseas real estate comes from the support of the local economy and population structure. The long-term development momentum of a city often determines the future performance potential of its real estate. Economic Stability and Growth Potential: Focus on whether the country’s overall economic structure is sound and whether its industries have the capacity for sustainable development. Population Flow Trends: Cities with net population inflows typically have more stable residential and rental demand. Urban Planning and Infrastructure Construction: The layout of transportation, commercial, and educational resources will affect the region’s attractiveness and future appreciation potential. Market Cycle Position Assessment: Understanding whether the real estate market is in an upward, stable, or adjustment phase helps in rationally timing market entry. At investment expos, many projects emphasize future potential, but investors still need to conduct independent research and long-term trend analysis to avoid making decisions based solely on short-term promotions. Legal System and Tax Differences Risks Cross-border investment means entering a completely different legal and regulatory system. Property structure, purchase procedures, and tax rules will all affect actual returns. Differences in Property Type: Freehold and leasehold ownership…

08/02/2026

08/02/2026

With accelerating globalization, investment immigration has become a key focus for an increasing number of high-net-worth individuals. Overseas investment not only allows for wealth allocation but also provides families with a better living environment and educational opportunities. However, investment immigration involves multiple stages, multi-departmental approvals, and varying national policy requirements, leading many to perceive the process as complex and time-consuming. Understanding the entire process and thorough preparation are crucial for successfully achieving overseas living and residency goals. Investment Immigration Policies and Project Selection Before deciding on investment immigration, it’s essential to clarify the policy requirements and available project types of the target country. Investment immigration programs vary significantly across countries; some focus on real estate, while others emphasize corporate investment or charitable donations. Each method has different financial thresholds and approval requirements. Project Type Differences: Real estate investment, corporate investment, and donations each have their own characteristics, with different financial thresholds and procedural requirements. Each country has specific requirements regarding the applicant’s age, education, health, and source of assets. Approval periods vary greatly; some countries complete the process in a few months, while others require more than a year. Meanwhile, leveraging professional consulting firms or legal teams can help you quickly understand projects that suit your circumstances and avoid getting bogged down in complex policies. Fund Verification and Legal Compliance Fund verification and legal review are among the most critical aspects of investment immigration and a major factor contributing to the time-consuming process. Applicants need to provide legal and traceable proof of the source of funds to ensure the compliance of investment funds. Different countries have different requirements regarding investment amounts, asset types, and fund transfers; some countries also require fund supervision through designated bank accounts. Furthermore, legal documents such as contracts, company registrations, real estate purchase or donation…

07/02/2026

07/02/2026

As global asset allocation concepts mature, overseas real estate investment is becoming an increasingly important focus for investors. At expos, overseas property projects are often touted as offering multiple benefits, including asset allocation, lifestyle planning, and educational opportunities. However, overseas real estate is not simply a matter of “buying a house”; it involves market environment, capital structure, legal systems, and long-term management. Thorough preparation before investment often determines whether a project is a sound asset or a potential burden. Clarifying Investment Objectives and Overall Planning Before actually engaging with overseas projects, investors must first clarify their investment objectives. Overseas real estate can be part of a long-term asset allocation strategy, or it may be related to family living, children’s education, or immigration planning. Different objectives necessitate entirely different selection logics. If the goal is asset preservation, mature markets and stable regions should be prioritized; if cash flow is emphasized, rental demand and holding costs need to be carefully considered; if family use is also taken into account, convenience and long-term living conditions must be considered. Only by clarifying objectives at the initial investment stage can subsequent market screening and decision-making remain on track. Understanding Overseas Market Environments and Institutional Differences The biggest difference between overseas real estate investment and domestic investment lies in the differences in market structure and institutional environment. These differences are often the main sources of risk. Market Environment Differences: Significant differences exist in the economic structure, population flow trends, and urban development stages of different countries, directly impacting long-term demand and value performance of real estate. Policy and Regulatory Changes: Overseas real estate policies may change with economic conditions or government policy adjustments, continuously affecting eligibility for purchase, holding costs, and transaction processes. Unfamiliarity with Legal Systems: Different countries have different legal systems and property…

05/02/2026

05/02/2026

Against the backdrop of continuously upgrading global asset allocation, overseas real estate is becoming a key investment focus for high-end investors. At various real estate exhibitions and investment expos, overseas properties consistently occupy a central position, attracting a large number of investors with an international perspective. They are not only concerned with the price fluctuations of the property itself, but also with long-term returns, asset security, and the possibility of global expansion. So, why do high-end investors continue to favor overseas real estate? The underlying investment logic and trends are the focus of this article. Overseas Real Estate Meets the Asset Allocation Needs of High-End Investors For high-net-worth individuals, investing in overseas real estate is a systematic asset allocation strategy, rather than a single investment choice. Diversifying Single Market Risk By allocating real estate assets in different countries and regions, the impact of regional economic fluctuations can be effectively reduced. Enhancing Asset Stability Real estate in mature overseas markets has strong long-term holding attributes, meeting the needs of high-end investors for stable asset allocation. Physical Assets Offer Greater Security Compared to financial products, real estate, as a physical asset that can be held for the long term, is more easily recognized by high-end individuals. Four Key Advantages: Clear Long-Term Value Preservation Potential Properties in prime locations of high-quality overseas cities often possess clear long-term value support. Comprehensive Advantages of Overseas Properties in terms of Returns and Planning High-end investors value not only the property price itself but also the multiple added values it brings. Stable Rental Return Expectations Long-term rental demand exists in some overseas markets, providing investors with a continuous cash flow. Balancing Self-Use and Investment Flexibility Overseas properties can be rented out for income or used as living or family space in the future. Facilitating a Globalized…

03/02/2026

03/02/2026

Driven by globalization, people’s pursuit of freedom, opportunity, and a better life has become increasingly intense. Traditional methods of obtaining citizenship often involve lengthy residency requirements, which to some extent restricts people’s movement. However, obtaining citizenship through investment is gradually becoming a new option for many, breaking down residency barriers and opening a door to a new life. Investment Citizenship: Breaking the Residency Shackles Traditionally, residency duration is a key indicator for obtaining citizenship. Many people have to abandon their original lives and jobs, leaving their homes to live long-term in their target country to meet residency requirements. This not only disrupts their original lifestyle but may also present challenges such as cultural differences and language barriers. Investment citizenship is entirely different; it does not require applicants to reside in the country long-term. Applicants only need to invest a certain amount of money according to regulations and meet relevant conditions to obtain citizenship. This means that people can obtain citizenship in another country without sacrificing their current life and enjoy the various rights of citizens in that country, such as education, healthcare, and social welfare. This flexibility makes investment citizenship an ideal choice for those who want to broaden their international horizons without giving up their current life. Diverse Investment Options to Meet Different Needs Investment citizenship programs typically offer various investment options to cater to the needs and preferences of different investors. Real estate investment is a common method; in some popular countries, purchasing property of a certain value allows one to apply for citizenship. This not only allows for capital gains but also provides a stable overseas asset. Business investment is another important pathway, where investors can participate in the operation of local businesses or create new ones, contributing to local economic development while achieving their citizenship…

31/01/2026

31/01/2026

In the investment field, diversification is a crucial strategy for mitigating risk and achieving stable returns. Including overseas real estate in an investment portfolio not only mitigates geographical risk but also leverages the differences in economic cycles across different markets to open new avenues for asset appreciation. So, how can overseas real estate be skillfully used to diversify an investment portfolio? Accurately Target Markets to Diversify Geographical Risk The global real estate market is vast, with varying stages of development, economic structures, and policy environments across different countries and regions. When choosing investment targets, it’s essential to avoid concentrating on a single region. For example, mature markets in Europe and America have well-established legal systems and stable real estate markets, suitable for investors seeking stable returns; while emerging markets such as Southeast Asia and the Middle East are in a phase of rapid development with significant economic growth potential and substantial real estate appreciation opportunities, suitable for investors with a higher risk tolerance. By diversifying real estate holdings across different regions, investments in other regions may remain stable or even appreciate when the market in one region fluctuates, effectively reducing the overall risk of the investment portfolio. Matching Different Property Types to Enrich Investment Dimensions Overseas real estate encompasses various types, including residential, commercial, and industrial real estate. Each type has its unique return model and risk characteristics. Residential properties typically offer stable rental income and potential capital appreciation, making them suitable for long-term holding. Commercial real estate, such as office buildings and shopping malls, offers higher rental yields but is significantly affected by economic conditions and the business environment. Industrial real estate is closely linked to manufacturing and logistics, experiencing strong demand during periods of economic prosperity. Investors can incorporate different types of properties into their portfolios based…

30/01/2026

30/01/2026

In today’s increasingly globalized world, people have broader perspectives on life, career, and asset allocation. Citizenship by investment, once a relatively niche concept, is gradually gaining mainstream attention and becoming an important choice for many to plan their future and expand their life’s horizons. So, what exactly is citizenship by investment? Definition and Forms of Citizenship by Investment Simply put, citizenship by investment is a way for individuals to obtain citizenship in a specific country by making a qualified investment. There are various forms of investment, with real estate investment being a common one. Investors purchase real estate of a specified value in the target country, hold it for a certain period, and then apply for citizenship if they meet relevant conditions. For example, some European countries stipulate that purchasing real estate of a certain value, holding it for several years, and meeting residency requirements can lead to citizenship. Government fund donations are also a form of investment. Some countries have established dedicated government funds, to which investors donate a certain amount of money in exchange for citizenship. The advantage of this method is its relatively simple process and the absence of concerns about the subsequent management and disposal of the property. Investment in commercial projects also attracts considerable attention from investors. Investors can obtain citizenship by investing in and establishing businesses or participating in existing commercial projects in a target country, creating jobs and driving economic development. This not only brings commercial benefits to investors but also contributes to local economic prosperity. The Historical Origins of Citizenship by Investment Citizenship by investment is not a new concept; its history dates back to the 1980s. At that time, some Caribbean countries pioneered similar programs to attract foreign investment and promote their economic development. These countries attracted numerous…

28/01/2026

28/01/2026

In international trade, finding stable and reliable overseas buyers is one of the most crucial tasks for foreign trade companies and export-oriented factories. While the widespread use of online platforms seems to offer more ways to acquire customers, in practice, truly high-quality overseas buyers with a strong willingness to close deals remain prevalent at offline trade shows. Various international and professional exhibitions have long been important venues for overseas buyers and crucial channels for foreign trade companies to expand into overseas markets. Finding overseas buyers through trade shows is not simply about “attending one show and getting orders.” The trade show channel is more like a systematic project, encompassing pre-show preparation and selection, on-site communication methods, and ongoing follow-up after the show. Many companies participate in trade shows year after year, but the results vary greatly. The reason often lies not in the trade shows themselves, but in whether they truly understand and utilize the characteristics of the “trade show channel.” Only with clear goals and appropriate methods can trade shows truly become an effective bridge connecting companies and overseas buyers. Choosing the Right Trade Show The first step in finding overseas buyers is choosing the right trade show. Different trade shows have vastly different focuses. Some emphasize brand showcasing, others prioritize procurement matchmaking, and still others lean towards industry exchange. When choosing a trade show, foreign trade companies shouldn’t just consider its size and reputation, but rather its alignment with their products and target market. Generally, highly specialized, industry-focused trade shows are more likely to attract genuinely interested international buyers. For example, specialized trade shows targeting a specific industry segment allow buyers to have clear objectives, leading to more efficient communication. In contrast, while general trade shows attract large crowds, the cost of customer screening is also higher. Clearly…

Number

NumberCall Now:

139 1723 4508

WeChat

WeChat

Form

FormBook Your Booth

Complete your information immediately and provide you with exclusive services!

Back to Top