-

Whatsapp

+1 689 248 1956 -

Email

joannewong0817@gmail.com

27/04/2026

27/04/2026

With increasingly diversified investment options and more complex information sources, many people tend to focus on only partial information when faced with different projects, lacking the ability to make overall judgments. Investment expos, by showcasing multiple industries and different types of investment projects in a unified setting, integrate information previously scattered across various platforms, allowing visitors to quickly build a basic cognitive framework. Furthermore, these events provide project demonstrations and, through on-site exchanges and comparative analysis, allow investors to more intuitively understand market structures, thus contributing to improved investment awareness. Concentrated Information Display for More Systematic Understanding Presenting multiple projects simultaneously enhances overall understanding. Investment expos typically cover real estate, finance, and various other industry investment projects, exposing visitors to different investment types. Reduces the Impact of Fragmented Information on Judgment: Comparing different project structures in a unified environment helps build a basic investment framework. This approach leads to more complete understanding. On-site Exchanges Enhance the Depth of Investment Understanding Communication ensures information goes beyond the surface. Project representatives or advisors explain the sources of returns, risk structures, and operational logic. Interactive learning enhances information absorption efficiency Asking questions allows for a deeper understanding of specific investment details, reducing misunderstandings. This exchange deepens cognitive understanding. Multidimensional Comparative Optimization of Investment Judgment Capability Horizontal comparison clarifies differences. Different projects are presented simultaneously in terms of returns, cycles, and risks, facilitating comparative analysis. The analysis process improves judgment:combining one’s own capital and risk appetite to select projects helps in forming rational decisions. This approach optimizes investment decisions. In the environment of an investment expo, information acquisition is no longer fragmented reception but rather a systematic understanding formed through centralized displays and interactive exchanges. Visitors can encounter multiple investment logics in a short time and gradually understand market differences through…

24/04/2026

24/04/2026

In the investment process, policy factors often directly impact project feasibility and future returns. However, relevant policy content is usually scattered and technically presented, making it easy for ordinary investors to misunderstand when researching on their own. Investment exhibitions, by showcasing different projects and industry information in a centralized manner, coupled with on-site explanations and consultations, provide visitors with opportunities to understand the policy background. In the same setting, the policy environments involved in different projects are systematically presented, allowing visitors to further understand their actual impact through interaction. This approach helps transform abstract policy content into more easily understood information, thereby improving overall judgment. Centralized Display Makes Policy Information More Accessible The gathering of multiple projects brings diverse policy content. Investment exhibitions typically cover multiple industries and fields, with each project involving corresponding policy background explanations. Simultaneously, centralized information reduces the difficulty of searching; visitors can encounter different policy content in the same setting without having to search separately. This method improves information acquisition efficiency. On-site Explanations Help Understand Policy Meaning Professional explanations make the content clearer. Project representatives or relevant personnel will explain the policy environment, helping to understand its impact on investment. The interaction process enhances understanding: Asking questions allows for a deeper understanding of policy details and scope of application, avoiding misunderstandings. This interaction makes policy information more concrete. Multiple comparisons improve judgment accuracy Different policy environments create a comparative framework. At the exhibition, policy differences between different projects or regions can be compared to determine their respective advantages. Combining policy conditions with investment objectives allows for a more rational assessment of project value. This approach makes decision-making more robust. In the environment of investment exhibitions, policy information is no longer fragmented and difficult to understand, but gradually becomes clear through display and…

23/04/2026

23/04/2026

Against the backdrop of increasingly complex real estate market information, homebuyers and investors face a growing number of choices. Significant differences exist between countries, cities, and projects, making it easy to arrive at incomplete or inaccurate judgments if relying solely on online information. Real estate exhibitions, by showcasing multiple projects in a single setting and providing opportunities for face-to-face interaction, allow participants to acquire more complete information in a unified environment. This direct and efficient approach makes exhibitions increasingly attractive for market research, enabling clearer decision-making. Information Concentration Improves Efficiency Simultaneous display of multiple projects reduces information fragmentation. Real estate exhibitions typically bring together real estate projects from different regions and types, allowing visitors to acquire a wealth of information at once. Unified Presentation Facilitates Quick Comparison: Comparing prices, locations, and amenities in the same space helps in quickly filtering for target projects. This centralized approach improves information acquisition efficiency. Face-to-Face Communication Enhances Trust Direct communication makes information more authentic. Visitors can communicate face-to-face with developers or consultants to understand project details and the true situation, reducing information bias during interaction. Asking questions on-site further clarifies project conditions and potential advantages. This communication approach strengthens the foundation of trust. Multi-dimensional comparison aids rational selection Comparison at the same event makes differences clearer. Different projects are presented together at the exhibition, facilitating horizontal comparison from multiple perspectives. Selecting more suitable properties based on individual needs helps reduce impulsive decisions. This approach makes choices more rational. In the environment of a real estate exhibition, information acquisition no longer relies on a single channel but rather forms a complete experience through centralized displays and on-site communication. Visitors can learn about multiple projects in a short time and make clearer judgments through comparison and communication. This efficient and intuitive approach improves…

22/04/2026

22/04/2026

In the investment decision-making process, project risk assessment is a crucial step influencing the final choice. However, much risk information is often hidden within the complex project structure and market background, making it difficult to grasp comprehensively through a single channel. Investment exhibitions, by showcasing multiple projects in a concentrated setting and providing opportunities for on-site exchange and comparison, allow visitors to access a wealth of information in a unified environment. Combined with direct communication with project teams and multi-dimensional comparisons, this offline setting helps to present risk factors more concretely, thereby improving the clarity of judgment and providing investors with a more complete reference basis before making a decision. Concentrated Display Makes Risk Information More Transparent Presenting multiple projects side-by-side facilitates the observation of differences. Investment exhibitions typically showcase project background, financial structure, and operating models, giving visitors a preliminary understanding of the basic situation. Concentrated Information Reduces Missed Risk Points: Comparing multiple projects in the same setting makes it easier to identify potential differences and inconsistencies. This approach helps in the initial identification of risks. On-site Communication Supplements Key Risk Details Face-to-face communication enhances the depth of information. Visitors can ask project teams or advisors about investment cycles, return stability, and potential uncertainties. Asking questions about key issues allows for a deeper understanding of project risk control measures and response plans. This communication method improves information reliability. Multi-dimensional comparison enhances risk assessment capabilities Horizontal comparison makes the risk structure clearer. Different projects presented at the same exhibition allow for comparison in terms of profit models, capital security, and industry background. Analyzing differences improves judgment accuracy: Screening based on one’s own risk tolerance helps avoid high-risk or mismatched projects. This approach optimizes overall decision-making. In the environment of investment exhibitions, risk information is no longer scattered…

21/04/2026

21/04/2026

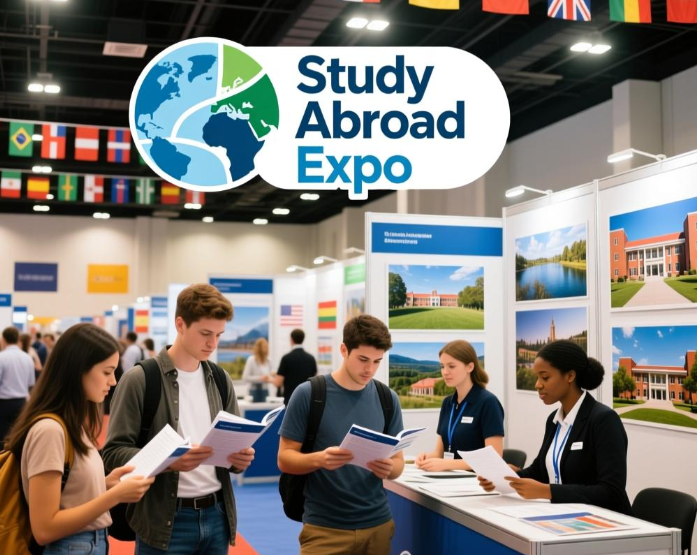

When planning their study abroad journey, many students focus on the courses and institutions themselves, but also consider the availability of internships and future practical resources. Overseas internship experience is often closely related to professional development and career paths, but relevant information is scattered, and searching individually can easily lead to missing key details. Study abroad expos, by showcasing institutional and program resources and providing on-site consultations, allow visitors to directly understand the internship arrangements and practical opportunities offered by different schools. This approach helps to concretize previously vague information and provides a reference for developing a more comprehensive study abroad plan. The institutional display shows the availability of internship resources Concentrated presentations make information more intuitive. At study abroad expos, some institutions will highlight their collaborations with companies, internship programs, or practical course arrangements. Students can compare the resource allocation of different schools to initially determine which institutions value practical opportunities. This approach helps build basic understanding. On-site Consultations Provide Specific Internship Details Face-to-face communication enhances the depth of information. Visitors can consult with admissions representatives or advisors to learn about internship acquisition methods, participation requirements, and related support services. Interactive communication clarifies information: Asking questions tailored to one’s professional field helps determine if internship opportunities match one’s needs. This communication method enhances the practicality of information. Multi-school comparison helps filter high-quality resources Horizontal comparison makes advantages more apparent. Different institutions differ in internship resources, partner companies, and practical opportunities. Comparison reveals key strengths. Analyzing these differences improves selection efficiency. Considering internship opportunities in conjunction with course content and career goals helps in selecting more suitable institutions, making decisions more rational. In the environment of a study abroad expo, overseas internship opportunities are no longer simply introduced but gradually presented in more detail through demonstrations and…

20/04/2026

20/04/2026

When planning their immigration, many people not only focus on policies and application requirements but also pay close attention to the living environment of their destination country, such as the quality of education, healthcare system, cost of living, and social atmosphere. However, relying solely on online information or scattered introductions often fails to provide a comprehensive understanding. Immigration expos, by showcasing immigration programs and lifestyle information from multiple countries and regions in a unified setting, allow visitors to quickly gain a more intuitive comparison and understanding, thus making a more systematic judgment on whether long-term residence and development are suitable. Multiple Country Showcases Highlight Differences in Living Environments Concentrated Information Makes Comparisons More Intuitive. Immigration expos typically cover programs from multiple countries and introduce basic information such as local education, healthcare, employment, and cost of living. Visitors can quickly compare the living conditions and residential characteristics of different countries in a single setting. This approach makes the differences more clearly visible. On-Site Consultations Provide Real-Life Details Exchanges Make Information More Specific and Credible. By communicating with immigration consultants or agencies, you can learn about the local community environment, climate characteristics, and convenience of life. Interactive learning enhances information depth: Asking questions tailored to individual needs helps determine if one is suited to the local lifestyle. This communication brings understanding closer to reality. Multi-dimensional information aids in holistic judgment It goes beyond focusing on a single factor, employing a comprehensive evaluation. Exhibition information typically covers policy conditions and living environments, allowing visitors to conduct overall comparative analysis. A holistic perspective improves judgment quality: Combining family needs with long-term planning allows for a more rational choice of a suitable country to live in. This approach makes decision-making more comprehensive. In the context of immigration expos, the living environments of…

18/04/2026

18/04/2026

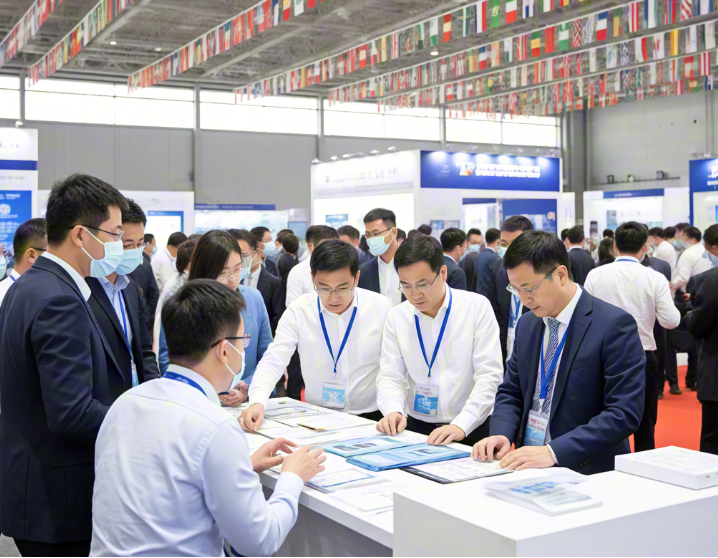

The 22nd WISE Property Expo wrapped up with great success from March 29 to 31 at the Shanghai World Expo Exhibition & Convention Center, marking another milestone for one of the industry’s most influential international real estate events. Over the course of three dynamic days, the expo brought together leading developers, agencies, and investment experts from across the globe. Exhibitors showcased a wide range of high-quality overseas property projects, covering key markets such as the United States, the United Kingdom, Australia, Canada, Southeast Asia, and more. The event attracted a large number of visitors, including investors, homebuyers, and families exploring international education and migration opportunities. The exhibition floor was vibrant and engaging, with attendees actively participating in face-to-face consultations, project presentations, and exclusive deal discussions. Many exhibitors reported strong interest and high-quality leads, reflecting continued demand for global real estate investment and diversification. In addition to property showcases, the expo also featured a series of professional seminars and forums. Industry experts shared insights on global market trends, investment strategies, immigration policies, and overseas education planning. These sessions provided valuable guidance for visitors navigating increasingly complex international markets. The success of the 22nd WISE Property Expo once again highlights Shanghai’s role as a key hub for global real estate exchange and investment. It also demonstrates the resilience and vitality of the overseas property sector in a changing economic landscape. With strong participation, high engagement, and positive feedback from both exhibitors and visitors, the event has set a new benchmark for future editions. Organizers have already begun preparations for the next expo, aiming to deliver an even more comprehensive and impactful platform for global property investment.The journey continues, and we look forward to welcoming you at the next WISE Property Expo.

18/04/2026

18/04/2026

When choosing a real estate project, many people face the problem of scattered information and inconsistent standards, making the judgment process complex. Different properties vary in price, location, and amenities, and without effective comparison, it’s easy to make a one-sided decision. Real estate exhibitions, by showcasing multiple types of properties in one space, bring previously scattered information together, allowing visitors to make multi-dimensional comparisons in a short time. Through on-site understanding and communication, the differences between properties are magnified, helping investors to more clearly judge their advantages and disadvantages and improve selection efficiency. Concentrated Display Makes Property Differences More Intuitive The same scene facilitates quick comparison. Different developers and projects are presented simultaneously at the exhibition, allowing visitors to directly compare prices, locations, and product types. Unified Information Reduces the Difficulty of Understanding: Observing under similar conditions makes it easier to discover the differences between properties. This method makes judging advantages and disadvantages more intuitive. On-site Communication Supplements Key Details Communication makes comparisons more in-depth. Through communication with project owners, you can understand the supporting facilities, development plans, and future development. Detailed information enhances judgment: Asking specific questions helps identify the strengths and potential weaknesses of a property. This interaction makes comparisons more comprehensive. Multi-dimensional analysis improves screening efficiency Property comparisons can be conducted from multiple perspectives, including price, location, and return potential, leading to a more complete understanding. Comprehensive judgment helps optimize choices. Screening based on one’s own needs allows for faster identification of suitable projects. This approach makes decision-making more rational. In the environment of real estate exhibitions, properties are no longer scattered information but are presented in a clear comparison through centralized display and exchange. Visitors can systematically analyze different projects through observation and communication, thereby more accurately judging their merits. This…

18/04/2026

18/04/2026

In a constantly changing investment environment, emerging industries often represent new growth opportunities. However, this information is usually scattered across different channels, making it difficult for ordinary investors to quickly and systematically capture trends. Investment Expo, by showcasing projects and companies from multiple sectors, present industries at different stages of development in a unified space, allowing visitors to observe market trends. Through on-site exchanges and information comparison, visitors can understand mature industries and gain easier access to growing emerging sectors, thereby improving their ability to judge future investment directions. Multi-Sector Showcases Present New Industry Trends Concentrated displays make emerging directions more intuitive. Investment Expotypically cover multiple sectors such as technology, energy, and finance, including many rapidly developing emerging industry projects. Concentrated information facilitates overall observation: Visitors can quickly identify which industries are in the growth stage through side-by-side comparisons. This approach helps capture market changes. Project Exchanges Provide Industry Development Information Communication makes trend judgments more concrete. Through exchanges with company representatives, visitors can understand the industry’s development background, technological advancements, and market prospects. Asking questions specific to a particular industry helps assess its development potential and risk structure. This approach improves the accuracy of understanding. Horizontal comparison helps identify potential industries Comparing multiple projects highlights differences. Simultaneous presentation of projects from different industries at the exhibition helps observe growth rates and resource investment. Combining market demand and development cycles makes it easier to screen for promising emerging industries. This approach optimizes investment direction. In the environment of investment Expo, emerging industries are no longer scattered information points, but gradually become clearer through concentrated displays and in-depth exchanges. Visitors can access development dynamics from multiple fields in a short time and form more comprehensive judgments through comparison and communication. This approach improves information acquisition efficiency, helps identify…

17/04/2026

17/04/2026

When choosing a school for studying abroad, the chosen major is often more crucial than the school’s name. The strengths of different institutions directly impact future learning experiences and career prospects. However, many students, in the initial information gathering phase, tend to focus only on the overall school introduction, overlooking the differences and details at the program level. Study abroad expos, by showcasing resources from multiple institutions and combining on-site explanations and consultations, allow visitors to more directly understand each school’s key disciplines and areas of strength. This face-to-face interaction makes program information more concrete and helps students more accurately determine whether a program aligns with their development goals, thus improving overall school selection efficiency. Concentrated Showcase Makes Strong Programs Clearer Multiple institutions presented together facilitate comparison. At study abroad expos, different schools highlight their strongest disciplines and unique program areas. Concentrated Information Reduces Screening Difficulty: Students can quickly compare the distribution of strong programs across multiple schools, rapidly building an initial understanding. This approach makes program information more intuitive. On-Site Consultation Deepens Program Understanding Face-to-face communication supplements detailed information. Visitors can directly consult with admissions representatives to learn about curriculum design, faculty strength, and career development paths. Interactive communication enhances understanding: Asking questions about areas of interest helps determine if a major aligns with personal plans. This communication makes information more specific and reliable. Multi-dimensional comparison aids in precise direction selection Horizontal comparison of the strengths of different schools and programs. The same major may have different focuses at different institutions; comparison helps identify a more suitable learning environment. Analyzing differences improves judgment efficiency: Comprehensive consideration of course content, practical opportunities, and career prospects helps in making more rational choices. This approach improves decision-making accuracy. In the environment of a study abroad expo, advantageous…

16/04/2026

16/04/2026

When making investment decisions, a project’s profit structure is often a crucial factor in determining its value. However, much information presented online is often generalized and lacks detailed support, making it difficult to fully understand. Investment Expo, by showcasing multiple projects and combining on-site explanations and interactive consultations, provide visitors with a more intuitive way to obtain profit information. In this environment, the sources, distribution methods, and influencing factors of different investment projects’ profits can be presented more clearly, making the originally abstract profit model more concrete, thus helping investors make more rational judgments and comparisons. On-site demonstrations make profit information more intuitive and clear Concentrated explanations make the structure easier to understand. At investment Expo, project teams typically demonstrate their profit sources and basic structure through materials, demonstrations, or explanations. Visitors can compare the profit models of different projects in the same setting, quickly establishing an initial understanding. This method makes the profit structure more visual. Face-to-face communication supplements detailed information Exchange makes the profit logic more complete. Visitors can directly ask project teams about key information such as the profit cycle, risk factors, and distribution rules. For complex revenue structures, on-site explanations can further clarify their operational logic. This interaction enhances the credibility of information. Multiple project comparisons improve judgment accuracy Horizontal comparisons make differences more apparent. Displaying different projects in the same setting facilitates observation of the differences and characteristics between revenue structures. By comprehensively analyzing revenue levels and risk factors, project value can be judged more rationally. This approach improves overall decision-making efficiency. In the context of investment Expo, revenue structures are no longer abstract concepts but are gradually clarified through demonstrations and communication. Visitors can understand the revenue models of multiple projects in a short time and deepen their understanding through comparison and…

15/04/2026

15/04/2026

When planning an immigration path, information acquisition costs are often overlooked but have a significant impact. Different countries have complex policies and diverse program types. Relying on a single channel to search for each program is not only time-consuming but also prone to fragmented information and difficulties in comparison. Immigration expos, by showcasing multiple countries and different types of immigration programs, bring previously scattered information together in a single setting, allowing visitors to quickly gain an initial understanding and make selections. Considering the presentation format of relevant immigration expo platforms, this offline, centralized consultation and matchmaking model does indeed have a significant advantage in information acquisition efficiency, thereby reducing overall information costs to some extent. Centralized Display Reduces the Cost of Multi-Channel Searches A Unified Setting Makes Information Acquisition More Efficient. Immigration expos typically bring together immigration programs from multiple countries and regions, allowing visitors to obtain basic information in one location. Initial information gathering can be completed without browsing multiple websites or institutions separately. This centralized approach significantly reduces information search costs. On-Site Consultation Improves Information Understanding Efficiency Face-to-face Communication Reduces Repeated Confirmation. Visitors can directly consult with immigration advisors or project representatives to understand policy details, application requirements, and procedures. They can ask questions on the spot about anything unclear, reducing the time spent on repeated inquiries later. This interactive approach improves information absorption efficiency. Multiple project comparisons shorten decision-making time and costs Comparisons at the same event make selection more intuitive. Different countries and projects are presented simultaneously at the expo, facilitating quick comparison of conditions and advantages. Through horizontal analysis, incompatible options can be eliminated more quickly, focusing on key choices. This comparison mechanism improves overall decision-making efficiency. In the context of an immigration expo, information is no longer scattered across…

Number

NumberCall Now:

139 1723 4508

WeChat

WeChat

Form

FormBook Your Booth

Complete your information immediately and provide you with exclusive services!

Back to Top