-

Whatsapp

+1 689 248 1956 -

Email

joannewong0817@gmail.com

09/03/2026

09/03/2026

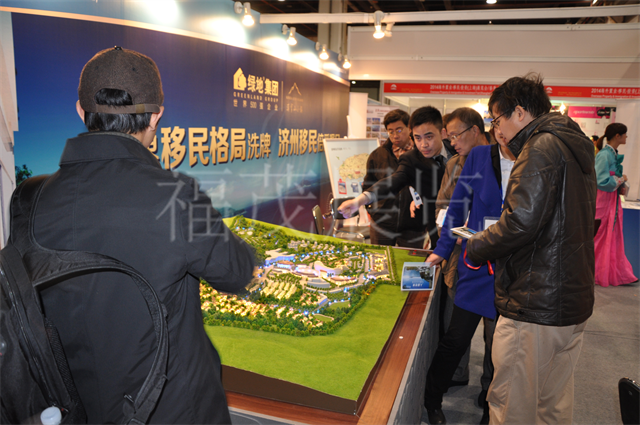

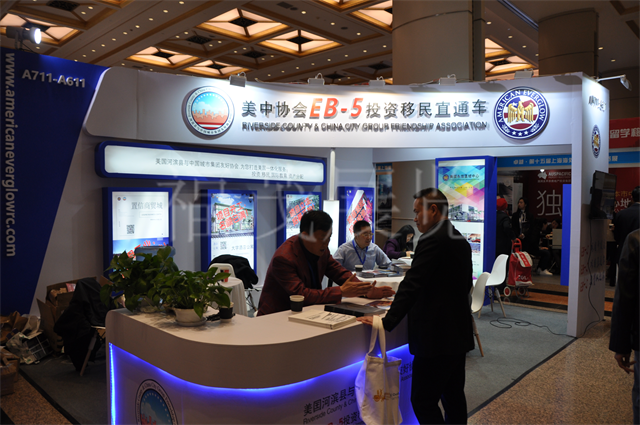

With the development of globalization, more and more families are paying attention to investment immigration and hope to obtain overseas residency or citizenship through financial investment. Investment immigration is not only related to identity planning but also involves asset allocation and long-term family development. Therefore, “how much money is required for investment immigration” has become one of the most common questions for people exploring such programs. Requirements vary widely between countries, and the total budget depends on investment thresholds, investment methods, and additional related costs. Investment thresholds vary by country Countries offer different investment immigration programs in order to attract international capital and talent, so the required investment amounts can differ significantly. Some countries set relatively low investment thresholds to attract international investors, with requirements starting at around $100,000 to $200,000. In several European countries, investment immigration programs are often linked to real estate purchases, with investment levels typically ranging from $250,000 to $500,000. In certain developed economies where demand is high, the investment requirement may exceed $500,000. Some programs require investors to maintain the investment for several years before they become eligible to apply for permanent residency or citizenship. Different investment options require different capital amounts Investment immigration programs usually offer several investment pathways, and the required capital depends on the type of investment chosen. Real estate investment: Purchasing property in the destination country is one of the most common options. Business investment: Establishing or investing in a local company to support economic development while meeting immigration requirements. Government funds or donations: Some programs allow applicants to contribute to government development funds. Financial investments: In certain countries, applicants may invest in government bonds or approved financial products. When choosing an investment option, it is important to evaluate factors such as financial security, investment duration, and potential returns. …

09/03/2026

09/03/2026

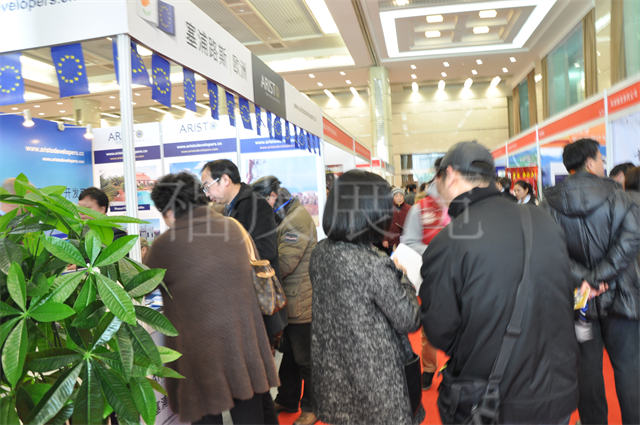

Overseas real estate investment is receiving increasing attention in global asset allocation. Real estate markets in different countries often have varying development potential and price ranges. Many investors hope to preserve the value of their assets, generate rental income, or achieve long-term appreciation by purchasing property abroad. However, cross-border investment involves far more factors than property prices alone, and uncertainties may arise from policies, regulations, and market environments. Many investors gather information about different national markets and investment rules when attending international real estate exhibitions in order to evaluate potential risks more comprehensively. Investment Risks Caused by Differences in Market Environments The operating logic of real estate markets varies significantly from country to country. Without sufficient understanding, investors may easily misjudge potential returns. Different stages of economic development mean that property prices in some cities may grow rapidly, but this can also be accompanied by market volatility. Changes in population structure can influence housing demand; for example, cities with strong population inflows often have greater long-term potential. Urban planning and infrastructure development can have long-term effects on regional property values. The size of the local rental market and tenant demand directly affect the actual income potential of a property. Uncertainty Caused by Policy and Regulatory Changes Overseas real estate investment is often influenced by national policies, and regulatory adjustments may change investment costs or transaction methods. Some countries restrict property purchases by foreign investors, so eligibility requirements must be confirmed in advance. Property taxes, land taxes, and holding costs vary significantly between countries. Certain regions may regulate short-term rentals, property resale, or capital transfers. Policy changes may affect the investment return cycle, making long-term policy monitoring important. Legal System and Transaction Process Risks Cross-border property transactions involve different legal systems. Without a clear understanding of these rules, potential…

06/03/2026

06/03/2026

With the deepening of international educational exchanges, more and more families are paying attention to overseas study opportunities. Different countries possess unique education systems, academic resources, and cultural environments, making studying abroad an important way to broaden horizons and enhance competitiveness. At various study abroad expos, students and parents often ask the same question: Which students are suitable for studying abroad? In fact, whether studying abroad is suitable depends not only on grades, but also closely related to learning goals, personal abilities, and future development plans. Students with Clear Learning Goals For students with a clear learning direction, overseas educational environments often offer more development opportunities. Clear Professional Direction: Having identified their desired field of study, such as finance, engineering, art, or international trade. Pursuit of High-Quality Educational Resources: Desiring access to more advanced teaching concepts, experimental facilities, or research platforms. Desire to Improve Language Skills: Improving foreign language application skills through a long-term immersive learning environment. Clear Career Plans: Hoping to work in international companies or multinational industries in the future. When learning goals are clear, studying abroad makes it easier to maintain sustained motivation and accumulate academic achievements. Students with independence and adaptability Studying abroad is not only a learning process but also the beginning of independent living. The ability to adapt to a new environment often impacts the entire study abroad experience. Strong self-management skills: Able to reasonably manage study time and life rhythm. Adaptability to new environments: Able to gradually adapt to different cultures, diets, and lifestyles. Good communication skills: Willing to actively communicate and integrate into new learning and social environments. Stable psychological resilience: Able to maintain a positive attitude when facing academic pressure or cultural differences. Students with strong adaptability are generally more likely to thrive in overseas environments. Students who wish…

05/03/2026

05/03/2026

Against the backdrop of a growing global trend towards residency planning and asset allocation, investment immigration has become a focal point for many families. Whether at immigration expos or various overseas investment exchange activities, the question “Is investment immigration really reliable?” is consistently asked frequently. Some value the travel and educational conveniences that residency brings, while others worry about policy changes and the risk of financial security. Determining the reliability of investment immigration requires a rational analysis from multiple perspectives, including policy stability, financial compliance, and long-term planning value. Policy Foundation and Legal Compliance The reliability of an investment immigration project hinges on its policy origins and legal foundation. Is it an officially recognized project? It should be confirmed that the project is formally established by the government of the target country, rather than being a product packaged by market intermediaries. Policy transparency and historical continuity: Projects with a long history and clearly defined rules are generally more stable. Is the approval process standardized? Are procedures such as background checks and verification of the source of funds open and transparent? Does it have a legal protection mechanism? Are the investment contract and residency application process protected by local laws? After obtaining project information from immigration expos, independently verifying the policy sources is a crucial step in mitigating risk. Fund Security and Risk Assessment Investment immigration often involves substantial financial investments, making fund security a key factor in assessing reliability. Clarity of Fund Purpose:Is the flow of investment funds clear, and are there any regulatory or escrow mechanisms in place? Fund Source Verification Requirements:Legitimate projects typically require proof of legal fund sources to ensure compliance. Additional Fee Risks: Understand the associated costs, such as intermediary service fees, legal fees, and other related expenses. Policy Adjustment Risk Assessment: Investment thresholds or…

04/03/2026

Against the backdrop of increasingly diversified global asset allocation, overseas real estate investment has become a key focus for more and more families. What truly determines the success or failure of an investment is not just the project itself, but the appropriateness of the city selection. Different countries and cities differ significantly in economic structure, population trends, and policy environment; choosing the right city often means a more stable foundation for returns. At real estate exhibitions, investors can access projects from multiple countries and cities, but how to make a rational judgment among numerous options is a crucial question to consider before cross-border property investment. Assessing Economic Strength and Development Potential A city’s long-term economic foundation is a crucial support for the stability of real estate values. A robust industrial structure: Cities with diversified industries generally have stronger resilience to risks. Employment and income levels: Regions with ample job opportunities and stable resident incomes are more likely to generate sustained housing demand. Internationalization: Cities with a high concentration of international companies often attract immigrants and long-term rental demand. Future planning direction: Government development strategies, key industry layouts, and large-scale infrastructure projects can all influence a city’s long-term potential. After obtaining city information from real estate exhibitions, cross-validating it with macroeconomic data and publicly available planning information helps avoid focusing solely on superficial promotional materials. Population Flow and Housing Demand Analysis The core logic of real estate always revolves around “people.” Whether a city has a continuous inflow of population is a key indicator of demand stability. Population Growth Trend: Cities with a continuous net inflow have a more solid foundation for housing demand. Proportion of Young Population: A high proportion of young workers usually means a more active rental market. Education and Living Resources: Areas with excellent schools, medical…

03/03/2026

03/03/2026

In today’s increasingly globalized world, more and more high-net-worth families are paying attention to the concept of “second citizenship.” Whether in asset allocation, children’s education planning, or international travel and business expansion, the impact of citizenship is being re-examined. Especially at immigration expos, second citizenship is often a focal point of discussion. It’s not just a passport, but a cross-border option and a long-term strategic tool. So, what are the practical benefits of second citizenship? Freedom of Travel and Global Convenience The most direct value of second citizenship lies in the convenience of international travel. Increased Visa-Free or Visa-on-Arrival Countries: Holding a passport from certain countries allows visa-free entry to many countries and regions, reducing visa application time and uncertainty. Improved Business Efficiency: Entrepreneurs who frequently engage in international business activities can arrange cross-border travel more flexibly. Greater Response to Unexpected Situations: In the event of changes in the international situation or emergencies, having an additional citizenship means more travel and residence options. Family Members Benefit Simultaneously: Most second citizenship programs allow spouses and children to obtain citizenship together, increasing overall freedom of travel. Convenient travel not only saves time but also provides greater flexibility for a global lifestyle. Expanded Education and Living Resources The advantages of citizenship extend beyond travel convenience; they can also be reflected in education and social resources. Expanded Educational Choices: Children can enjoy the same educational opportunities as local students in their country of citizenship, with greater flexibility in school applications. Optimized Education Costs: Tuition fees for local students are significantly lower than for international students in some countries. Healthcare and Social Security Systems: Legal citizens typically enjoy access to local public healthcare and some social welfare systems. Long-Term Residence and Development Opportunities: Families can live or work in different countries according to their…

02/03/2026

02/03/2026

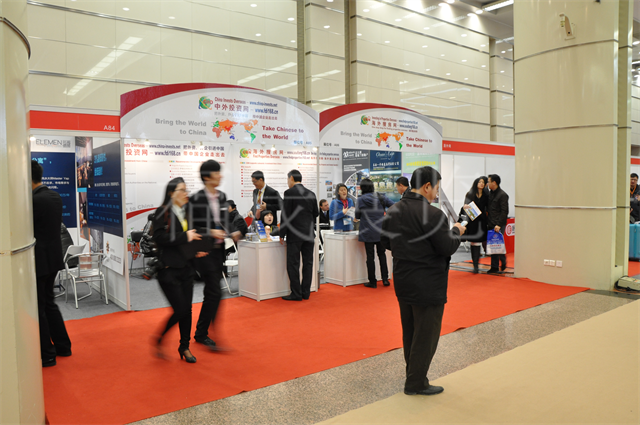

With the global trend towards asset diversification, more and more investors are focusing on overseas real estate markets. Compared to domestic property purchases, cross-border property investment involves more complex processes and rules. From project selection and funding arrangements to legal compliance and post-investment management, each step is crucial to the success or failure of the investment. Many people learn about projects in different countries through real estate exhibitions, but a clear understanding of the entire process is still necessary when actually implementing the investment. Mastering the key steps of overseas real estate investment helps improve efficiency, reduce risks, and make cross-border asset allocation more stable. Preliminary Research and Project Selection Before making a formal investment, thorough research is an indispensable step. Different countries vary significantly in terms of economic environment, policy stability, and market maturity. Choosing a market that suits one’s own goals is particularly important. Define your investment goals: Differentiate whether you are pursuing asset appreciation, rental income, or considering residency and education planning. Different goals determine different market choices. Compare the fundamentals of countries and cities: Analyze economic growth, population flow, and industrial development trends to assess long-term potential. On-site or online project inspection: Obtain information through real estate exhibitions or project briefings, and combine this with independent research for screening. Assess developer and project qualifications: Review historical project performance and credit records to reduce development risks. The core of this stage lies in information integration and judgment, not hasty decisions. Funding Arrangements and Transaction Process After identifying the target project, the actual transaction stage begins. Overseas real estate transaction processes differ significantly from those in the domestic market, requiring prior understanding of the requirements at each stage. Funding preparation and remittance arrangements: Confirm the proportion of the purchase price, payment schedule, and cross-border fund compliance procedures….

28/02/2026

28/02/2026

Against the backdrop of a deepening global trend towards diversified asset allocation, overseas real estate has gradually become an important focus for investors. Whether for risk diversification, asset structure optimization, or paving the way for future family life and education planning, cross-border property investment carries a longer-term significance. However, different countries have significant differences in economic environment, legal system, tax system, and market cycle. Without a systematic understanding and prior preparation, investment risks may be underestimated. What should you pay attention to when investing in overseas real estate? A comprehensive understanding of key factors before making a move is an important foundation for achieving stable returns. Market Environment and Development Potential Assessment The value of overseas real estate comes from the support of the local economy and population structure. The long-term development momentum of a city often determines the future performance potential of its real estate. Economic Stability and Growth Potential: Focus on whether the country’s overall economic structure is sound and whether its industries have the capacity for sustainable development. Population Flow Trends: Cities with net population inflows typically have more stable residential and rental demand. Urban Planning and Infrastructure Construction: The layout of transportation, commercial, and educational resources will affect the region’s attractiveness and future appreciation potential. Market Cycle Position Assessment: Understanding whether the real estate market is in an upward, stable, or adjustment phase helps in rationally timing market entry. At investment expos, many projects emphasize future potential, but investors still need to conduct independent research and long-term trend analysis to avoid making decisions based solely on short-term promotions. Legal System and Tax Differences Risks Cross-border investment means entering a completely different legal and regulatory system. Property structure, purchase procedures, and tax rules will all affect actual returns. Differences in Property Type: Freehold and leasehold ownership…

27/02/2026

27/02/2026

Against the backdrop of deepening global asset allocation, overseas real estate investment has become a key topic of concern for many high-net-worth individuals. Whether at real estate exhibitions or investment expos, the question of “Are overseas real estate returns high?” is consistently raised. Some value stable rental income, others anticipate asset appreciation, and still others view it as a long-term asset preservation tool. Given the differences in market environments and policies across countries, the true returns of overseas real estate require rational analysis from multiple perspectives. Market Growth Potential and Asset Appreciation Potential To determine whether overseas real estate investment returns are ideal, the first step is to examine the long-term growth potential of the target market and regional development trends. Economic and Population Growth Drivers: Cities with stable economic growth and continuous population inflows often provide long-term demand support for real estate. Differences in City Development Stages: Emerging cities in a growth phase may have greater appreciation potential, while mature markets tend to favor steady growth. Infrastructure and Planning Advantages: Transportation construction, improved commercial facilities, and government development plans all contribute to driving up property values. Supply and demand affect prices: Areas with limited supply and strong demand are more likely to see price increases. Under sound fundamentals, overseas real estate can indeed bring considerable asset appreciation, but returns are often based on long-term holding and proper location selection. Rental Income and Cash Flow Performance Besides price appreciation expectations, many investors are more concerned about rental yield and cash flow stability. Rental Market Maturity: Markets with stable rental demand and well-established management systems are more conducive to achieving continuous rental income. Significant Differences in Returns: Rental yields vary considerably across different countries and cities, requiring a comprehensive assessment considering both property prices and rental levels. Holding Costs: Taxes,…

26/02/2026

26/02/2026

In today’s rapidly globalizing world, investment immigration has become a significant option for an increasing number of high-net-worth families. Beyond asset allocation and residency planning, many are more concerned with the tangible benefits of investment immigration: freedom of travel, access to educational resources, wealth protection, and an upgraded lifestyle. As residency becomes more than just a residence permit, but an integral part of a global strategy, the comprehensive advantages of investment immigration are being reassessed by a growing number of rational investors. Increased Freedom of Travel and Residence The most noticeable changes after obtaining overseas residency are often in travel and residence arrangements. This freedom significantly facilitates family life and business dealings. Visa Convenience and Travel Advantages: Holding residency or citizenship in several countries allows for visa-free or simplified visa processes to multiple countries, greatly improving international travel efficiency. Long-Term Residence Options: Investment immigration typically grants applicants long-term residency or permanent status, allowing them to freely choose their place of residence based on family plans. Facilitated Global Business Travel: For entrepreneurs, overseas residency helps expand into international markets and reduces the time and administrative costs of business travel. Four key benefits for family members: Spouses and children typically obtain residency status simultaneously, allowing for greater flexibility in family travel and residence arrangements. This convenience extends beyond daily life, creating smoother pathways for cross-border investment, overseas property ownership, and international cooperation. Education and Social Resource Advantages Beyond the change in residency status, the long-term advantages of investment immigration for families are primarily in education and social resources. Priority access to education resources: After obtaining local residency, children typically enjoy greater advantages in school admissions, tuition fees, and educational choices. Optimized education costs: In some countries, local residents can enjoy lower tuition fees or more scholarship opportunities. Healthcare and social security:…

25/02/2026

25/02/2026

In today’s increasingly globalized asset allocation landscape, more and more high-net-worth individuals, business owners, and cross-border families are focusing on overseas real estate investment. In the past, people purchased overseas real estate primarily for reasons of residence, education, or asset preservation. However, with the increasing transparency of international tax rules, the implementation of the CRS information exchange mechanism, and the emergence of differences in tax burdens between domestic and international markets, the function of overseas real estate has evolved from a single investment tool to a comprehensive tax planning vehicle. Properly allocating overseas real estate can not only diversify asset risk and hedge against exchange rate fluctuations, but also optimize the burden of personal income tax, corporate income tax, inheritance tax, and capital gains tax, all within legal and compliant boundaries. Tax planning is not simply “tax avoidance,” but rather, within the bounds of the law, achieving a balance between minimizing tax burdens and maximizing cash flow through arrangements of ownership and timing. Overseas real estate, with its strong tangible asset attributes, stable valuation, and relatively clear policies, is naturally suited as a core element in tax planning. Whether held through a company, a trust structure, or through immigration planning and residency arrangements, overseas real estate can serve as a bridge connecting tax system differences. Tax Rate Differences Different countries have significantly different standards for levying property-related taxes. Some countries have no property tax or extremely low tax rates, while others offer long-term tax exemptions. For example, some countries do not levy capital gains tax or have low holding taxes. Investors can effectively reduce long-term holding costs by holding property in low-tax jurisdictions. From a planning perspective, allocating major assets in low-tax jurisdictions is equivalent to a natural “tax reduction.” Long-term rental or transfer results in a higher overall…

25/02/2026

25/02/2026

With the increasing popularity of global asset allocation concepts, more and more families and investors are turning their attention to overseas real estate markets. Whether for children’s education, immigration, asset preservation, or seeking higher rental returns and long-term appreciation potential, overseas property purchases have become an important part of cross-border investment. However, compared to domestic property transactions, overseas property purchases involve completely different legal systems, property rights structures, transaction processes, and regulatory environments. Language differences, cultural differences, and asymmetric legal information often put buyers at a disadvantage. Ignoring key risk points can lead to issues ranging from affecting the use of property rights and realizing returns to serious consequences such as financial losses, property disputes, and even protracted litigation. More importantly, different countries have different restrictions on foreign investors. Some countries have strict regulations on land holding, foreign investment ratios, tax declarations, and even the source of funds. Without professional legal and compliance awareness, relying solely on intermediaries or developers can easily lead to risks such as “contract traps,” “defective property rights,” or “policy violations.” Therefore, risk prevention should precede investment decisions in the overseas property purchase process. Through preliminary investigation, professional consultation, standardized transactions, and ongoing compliance management, legal risks can be minimized, truly achieving asset security and stable returns. Understanding Local Regulations Before formally viewing properties or signing contracts, it’s crucial to research the real estate legal framework of the target country. Each country has different regulations regarding foreign home purchase qualifications, land ownership forms, and transaction approval procedures. Some countries allow freehold ownership, while others only offer long-term leasehold ownership. Without prior understanding, you may end up buying a property with a limited lease term. It’s recommended to consult official regulations or local lawyers, rather than simply relying on sales pitches. Mastering basic legal…

Number

NumberCall Now:

139 1723 4508

WeChat

WeChat

Form

FormBook Your Booth

Complete your information immediately and provide you with exclusive services!

Back to Top