-

Whatsapp

+1 689 248 1956 -

Email

joannewong0817@gmail.com

16/01/2026

16/01/2026

When it comes to studying abroad, many people’s first thought is still the traditionally popular destinations like the UK, US, Australia, and Canada. However, in recent years, the term “study abroad on a less popular path” has been increasingly mentioned, with some parents and students turning their attention to European countries with less commonly spoken languages, Northern Europe, Eastern Europe, Southeast Asia, and even Latin America. Some believe this is a cost-effective and less competitive option, while others worry about lower school reputation, language barriers, and insufficient recognition upon returning home. It’s important to note that studying abroad on a less popular path doesn’t mean studying anywhere, nor is it a compromise. It’s more like a path different from the mainstream, but one that can still be successful. Is studying abroad on a less popular path truly more cost-effective? This is a question many people are most concerned about. Compared to popular destinations, less popular study abroad destinations are indeed more affordable in terms of tuition and living costs. Some countries have lower tuition fees for public universities, sometimes only requiring a registration fee, significantly reducing the overall financial burden. However, cost-effectiveness isn’t just about being “cheap”; it also depends on the quality of learning, the strength of the program, and personal gains. If you choose a university with a strong program and a mature teaching system, the return on investment for studying abroad on a less popular path is often higher. Will a less prestigious university affect future career prospects? Many people worry that universities in less-known countries may not be as well-known as top-tier universities, and wonder if this will be a disadvantage upon returning home. In reality, employers value professional skills, practical experience, and overall qualities more than just a university’s reputation. If a university is…

16/01/2026

16/01/2026

“Following the crowd” in studying abroad means seeing others choose a particular country, school, or major and then applying to the same one. While it may seem convenient and trendy, the risks are obvious: the child may not be suited, the money spent may not meet expectations, and the degree and experience may not be relevant upon returning home. As parents or students, before making a decision, put aside concerns about “face” and “conformity” and ask yourself several practical questions: What does the child truly enjoy? What costs can the family afford? What future career path do they want? Avoiding following the crowd doesn’t mean rejecting others’ experiences, but rather turning their successes or failures into valuable information for your own decision-making. Clarify the Child’s Interests and Abilities Many decisions based on following the crowd stem from the mindset of “I’ll do what others do.” Stop and ask two questions: What does the child enjoy learning? What kind of educational model suits the child’s personality, language skills, and learning habits? Interest determines motivation, and ability determines feasibility. Make the goals specific—is it for academic advancement, career preparation, language improvement, or life experience? Different goals correspond to different countries, different types of schools, and different programs. Assessing the Match Between School and Program While prestigious universities are attractive, they are not the only criterion. Consider the program’s strength, curriculum, teaching methods, faculty resources, and practical opportunities. For example, a school might rank highly in business, but if your child wants to study art or engineering, reputation isn’t the most crucial factor. Also consider the language of instruction, program length, internship and employment support, and post-graduation recognition. Matching the “school-program-student” relationship is more effective than simply looking at rankings or “popular countries.” How to get real information The source of…

16/01/2026

16/01/2026

In recent years, studying abroad has become an important investment for many families’ future. However, with the development of the global education market and the continuous rise in the cost of living, the question of “Will the cost of studying abroad continue to rise?” has become a major concern for parents and students. Some worry that future costs will become increasingly high, placing a heavy burden on their families; others are considering whether there are ways to control costs in advance and make studying abroad more affordable. In fact, whether the cost of studying abroad will rise, and the speed and extent of that rise, are affected by many factors, such as exchange rate fluctuations, inflationary pressures, the popularity of studying abroad, and policy adjustments, some of which are unpredictable. However, through reasonable planning and strategic arrangements, it is possible to control overall expenditures to a large extent, ensuring that studying abroad is “spent wisely and worthwhile.” Will the cost of studying abroad really continue to rise? Many families worry that “the cost of studying abroad will rise like housing prices indefinitely.” In fact, while the trend of studying abroad costs is upward, it is not unidirectional and unlimited. University tuition and accommodation fees are affected by school policies, government regulations, and market competition; living expenses are closely related to local price levels and exchange rates. To attract international students, some countries may implement more flexible tuition policies or provide support measures, which can mitigate the rate of cost increases. Therefore, rather than panicking, it’s more important to focus on the cost trends of your target country and specific schools, rather than simply assuming “it will definitely be more expensive in the future.” Which costs are most likely to rise? Which are controllable? Many study abroad expenses can be…

16/01/2026

16/01/2026

As studying abroad becomes an increasingly popular option for families planning their children’s future, explicit expenses such as tuition and accommodation fees are already included in the budget. However, what truly catches many families off guard are often the “hidden costs” concealed in visa applications, daily life details, and even cultural adaptation. From flight rescheduling fees to international medical insurance, from textbook printing costs to cross-cultural social expenses, these seemingly disparate expenses can accumulate and exceed the total cost of studying abroad by more than 30%. Unveiling the truth behind these hidden costs is crucial for making study abroad plans more rational and avoiding “economic overspending” that could negatively impact academic performance and quality of life. Visa and Administrative Costs: A Chain of Expenses from Document Notarization to Immigration Bureau “Express Fees” Applying for a student visa is the first step in preparing for studying abroad, but the “hidden costs” of this step are often underestimated. Besides the visa application fee itself, many countries require document notarization (such as birth certificates and academic certificates), with a single notarization costing between 200-500 yuan. Translation doubles the cost. Some countries also require medical examination reports, and the fees at designated institutions are generally higher than at ordinary hospitals, plus additional vaccination fees. Even more problematic is the “expedited service”—if visa processing is needed due to insufficient materials or time constraints, the cost can range from several thousand to tens of thousands of yuan. One student, for example, failed to prepare a criminal record check in advance and only applied for expedited processing close to the start of the semester, ultimately paying 8,000 yuan in “express lane fees,” far exceeding their budget. Fluctuations in Living Costs: From “Supermarket Price Tags” to “Exchange Rate Traps” The cost of living varies greatly between countries where…

16/01/2026

16/01/2026

As the domestic real estate market enters a “slow cycle,” overseas properties, with their characteristics of risk diversification, stable rental income, and asset preservation, have become a “new blue ocean” for high-net-worth individuals’ asset allocation. From tropical beaches in Southeast Asia to historic cities in Europe, from technology hubs in North America to livable communities in Australia, the global real estate market offers investors a wealth of choices. However, legal differences, market volatility, and cultural barriers between countries make “choosing the right project” a skill. How to sift through a sea of options to find truly promising targets? The answer lies in the details of urban planning, population flow, rental returns, and risk management. Mastering these core logics is essential to accurately capture opportunities in global investment and achieve steady wealth growth. Urban Development Potential: Follow the “Growth Pole,” Avoid the “Shrinking” Trap The primary principle for choosing overseas real estate is to “bet on the city’s future.” Prioritize core cities, economic corridors, or emerging industry clusters in target countries or regions. These areas often benefit from policy support, infrastructure investment, and population inflows. For example, Bangkok and Ho Chi Minh City in Southeast Asia have seen sustained strong housing demand due to manufacturing relocation and the rise of the middle class; Berlin and Barcelona in Europe have experienced rising house prices and rents thanks to the recovery of the technology industry and tourism. Conversely, investing in “shrinking cities” experiencing population outflow and industrial decline may result in high vacancy rates, slow appreciation, or even depreciation. One investor purchased property in Detroit, but due to the relocation of the local auto industry leading to a sharp population decline, the property value ultimately shrank by 60%, and rental income could not cover maintenance costs. Democracy Structure and Demand: Capitalizing on the…

16/01/2026

16/01/2026

Amid the global asset allocation trend, overseas real estate has become a highly sought-after asset for high-net-worth individuals due to its advantages in risk diversification and inflation hedging. “Freehold ownership,” a core selling point of overseas real estate, is often packaged as a “one-and-done” wealth-building secret, attracting countless investors. However, property rights systems, holding costs, and legal risks vary significantly across countries. Blindly pursuing the “freehold” label can lead to investment traps. Unveiling the truth about the duration of overseas property ownership is the first step towards sound investment. Freehold Ownership: Not a “Safe Haven” Many believe that “freehold ownership” of overseas real estate means that the land and house can be passed down indefinitely, but this concept needs to be interpreted within the specific legal framework of each country. While there are no time limits for the use of real estate in the United States, owners are required to pay property taxes annually (usually 0.5%-2% of the assessed value). If taxes are overdue, the government has the right to auction the property to offset the taxes. For example, an investor who purchased a villa in California suffered significant losses because he failed to pay property taxes on time, resulting in the property being auctioned off by the government at 60% of the market value. Japan practices private land ownership, with both houses and land having permanent ownership rights. However, buildings themselves have “lifespan limitations”—while ordinary residential properties have no time limit, they require regular renovations due to earthquakes, aging, and other issues; otherwise, they may be deemed “dangerous” and forcibly demolished. Land ownership is retained, but the house’s value becomes zero. The UK divides ownership into “freehold” and “leasehold.” Freehold, such as detached houses, allows for permanent ownership of the land and house, while leasehold, such as apartments, typically…

15/01/2026

15/01/2026

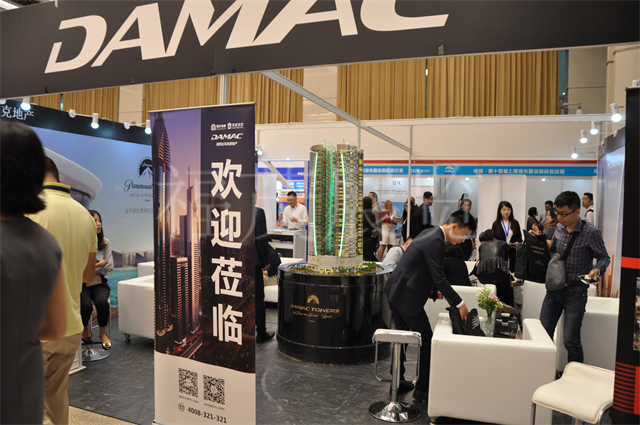

In the wave of global asset allocation, Dubai, with its unique policy advantages, robust economic growth, and continuous population inflow, is becoming a “value haven” in the eyes of global investors. The real estate market of this Middle Eastern business hub is undergoing a profound transformation from an “investment hotspot” to a “long-term asset allocation destination,” opening a window for investors that combines profitability and security. The attractiveness of Dubai’s real estate market stems first from its “zero-burden” policy framework. As one of the few regions globally with a freehold ownership system, buyers do not need to worry about expiration dates and there are no property taxes, land taxes, or other holding costs. Coupled with a registration fee of only 4%, the investment threshold is significantly lowered. More importantly, the “Golden Visa” policy continues to be upgraded—purchasing a property worth 2 million dirhams (approximately 4 million RMB) grants a 10-year residency permit, with down payments for off-plan properties reduced to 0%, and visa applications based solely on the contract. This policy not only attracts high-net-worth individuals but also makes real estate a preferred tool for obtaining a “second citizenship.” Data shows that since the policy’s implementation, Dubai has issued over 250,000 Golden Visas, directly boosting the proportion of owner-occupier buyers to 50% of transactions, shifting market demand from speculation to genuine residential needs. Economic diversification is the cornerstone of Dubai’s real estate market. While most global economies rely on a single industry, Dubai has built a multi-pronged economic system driven by finance, logistics, tourism, technology, and new energy. In 2024, non-oil industries accounted for over 75% of GDP, and the UAE’s overall non-oil foreign trade grew by over 24.5%, providing solid support for the real estate market. Emerging areas such as the Dubai Canal Corridor and the Dubai Archipelago have…

15/01/2026

15/01/2026

Studying abroad is a significant turning point in life. Choosing a country not only affects academic development but also future career paths and life experiences. However, faced with traditionally popular destinations like the US, UK, Australia, and Canada, as well as emerging destinations like Singapore, the Netherlands, and Germany, how does one choose the most suitable country? This involves not only academic development but also multiple factors such as cultural adaptation, career planning, and cost of living. From the match between personal interests and majors, the quality and resources of education, cultural inclusiveness and language environment, to the cost of studying abroad and employment prospects, each dimension needs to be comprehensively considered to find a study destination that truly meets one’s needs. The match between personal interests and majors is the primary basis for choosing a study abroad destination. Different countries have their own strengths in different academic fields: the US is known for its technological innovation and interdisciplinary research, with world-leading programs in computer science, artificial intelligence, and business management; the UK has a deep academic tradition, with strong programs in humanities and social sciences such as literature, history, and law; Germany is world-renowned for its engineering and manufacturing, with mechanical engineering and automotive design attracting a large number of STEM students; and Australia excels in environmental science, medicine, and education. If you’re interested in artistic creation, fashion design in Italy or fine arts in France might be more suitable; if you plan to enter the finance industry, hotel management in Switzerland or fintech courses in Singapore are more targeted. Choosing a country that highly matches your interests and career goals can stimulate learning motivation and lay a foundation for future career development. Educational quality and resources are core considerations. A high-quality education system is not only reflected in…

15/01/2026

15/01/2026

Amid the global asset allocation boom, overseas off-plan properties have become a top choice for many investors due to their price advantages, payment flexibility, and potential appreciation. However, unlike domestic property purchases, overseas off-plan properties involve multiple risks, including cross-border legal issues, exchange rate fluctuations, and developer qualifications. A slight misstep can lead to losing both money and property. How can one mitigate risks and maximize returns in overseas off-plan property investment? The key lies in grasping the core aspects, from developer qualifications to contract terms, from fund security to delivery and acceptance—each step requires careful attention. Developer qualifications are the primary consideration in overseas off-plan property investment. The maturity of overseas real estate markets varies greatly, and some emerging markets face the risk of developers experiencing cash flow problems and projects becoming unfinished. For example, in some Southeast Asian countries, developers have faced difficulties in financing, leading to the suspension of off-plan construction. Investors not only lose their down payment but also bear the subsequent costs of pursuing legal action. Therefore, when selecting a developer, it is crucial to examine their historical project delivery record, financial strength, and industry reputation. This can be achieved by checking local land bureau registration information, contacting owners of completed projects, or commissioning professional agencies to conduct due diligence to ensure the developer has legal development qualifications and a strong ability to fulfill contractual obligations. Furthermore, prioritize projects developed by listed companies or large real estate developers, as these companies typically have more abundant funds and stronger risk resistance. Contract terms are the core basis for protecting your rights. Overseas property purchase contracts are mostly in local legal texts, with complex language and detailed clauses. Investors need to review them word by word, paying close attention to key aspects such as payment methods, handover…

14/01/2026

14/01/2026

Every year, many students and parents who want to study abroad pay attention to various study abroad expos. When it comes to study abroad expos, many people might picture a bustling exhibition: universities and educational institutions from various countries displaying promotional materials, students consulting with information, and listening to lectures. However, the information that study abroad expos can provide goes far beyond the surface. It’s not just a window to understand institutions, but also an important place to obtain the latest policies, visa information, scholarship opportunities, and even future career planning. What countries and schools can I learn about? Many people ask, “What schools and countries can I learn about at a study abroad expo?” In fact, most expos invite universities, colleges, and language training institutions from all over the world to participate. You can directly communicate with school representatives face-to-face, asking about curriculum, tuition fees, admission requirements, academic environment, and other questions. This face-to-face communication is more intuitive than simply searching for information online and is more likely to provide personalized advice. Can I get study abroad policies and visa information on-site? Another common question is, “Policies change quickly; can I get the latest information at the expo?” The answer is yes. Many embassies and official study abroad agencies set up information booths at the expo, providing the latest visa application procedures, policy changes, and language test requirements. This helps applicants avoid delays due to outdated information. How many scholarships and financial aid opportunities are available? Many parents and students are concerned: “Study abroad is expensive; can I learn about scholarships or grants on-site?” At the expo, schools usually announce various scholarship policies, including application requirements, amounts, and deadlines. You can also get advice on preparing scholarship materials and enhancing your competitiveness, which is more comprehensive and…

14/01/2026

14/01/2026

In today’s environment of abundant information channels, many people ask: Is it really necessary to attend investment expos in person? With so much information online—reading news, browsing updates, and listening to live streams—it seems like you can learn a lot about investments. But actually attending an investment expo offers a completely different experience. Investment expos bring together project owners, investors, service providers, and policy information in a single space, creating a “high-density information field.” For investors, this is not just about viewing projects and listening to presentations, but also an opportunity to comprehensively understand market trends, validate judgments, and expand networks. Especially for ordinary and small-to-medium-sized investors, investment expos provide a relatively low-barrier, comparable, and communicative environment. What Investment Projects and Directions Can You Access All at Once? One of the biggest opportunities at investment expos is the concentrated display of projects. Projects from different fields and at different stages will be showcased at the same expo, covering multiple directions such as the real economy, technological innovation, consumption upgrades, and financial services. For investors, this concentrated display allows them to quickly understand market hotspots and areas of capital focus, without having to travel around. Even if they don’t invest immediately, they can develop a holistic understanding of industry trends by comparing different projects. Can I more directly assess the true nature of a project? Many investment opportunities online appear “perfect,” but lack authenticity. Expos offer face-to-face opportunities, allowing investors to communicate directly with project leaders and observe the team’s performance, communication skills, and professionalism. On-site Q&A and interaction often uncover details not found in promotional materials, which is extremely helpful in determining a project’s reliability. Will I have access to policies and authoritative information? Many investment expos invite relevant departments, industry associations, or research institutions to participate, providing…

14/01/2026

Investment immigration is not only a global asset allocation strategy but also a crucial decision for family future planning. The timing of the application process requires consideration of the cyclical fluctuations in the target country’s immigration policies, as well as a comprehensive assessment of personal assets, family needs, and market conditions. From Hong Kong to the United States, from Singapore to the United Kingdom, the policy dynamics and application timings of major global immigration destinations together constitute the “time code” for investment immigration. The optimization cycle of Hong Kong’s investment immigration policy provides investors with a clear “time anchor.” Since its resumption, Hong Kong has continuously lowered the threshold through multiple rounds of policy adjustments. For example, the investment threshold for residential properties has been reduced from HK$50 million to HK$30 million, while the upper limit for non-residential properties included in the investment has been raised to HK$15 million. Such policies are typically implemented gradually after the government’s policy address is released, creating a peak application period of 3-6 months. For example, in the three months following the policy adjustment in September 2025, the number of applications received by the Hong Kong Immigration Department increased by 40% month-on-month, with a corresponding increase in the approval rate. For applicants meeting the asset requirements (holding HK$30 million in net assets for six consecutive months), the first quarter after the policy takes effect is the optimal window of opportunity—the approval process is more efficient at this time, and priority can be given to selecting high-quality investment targets, avoiding asset premiums caused by increased competition later. The “policy bonus period” for US investment immigration is strongly correlated with the backlog of applications and the validity period of the legislation. The “grandfather clause” of the EB-5 investment immigration program stipulates that investors who submit their…

Number

NumberCall Now:

139 1723 4508

WeChat

WeChat

Form

FormBook Your Booth

Complete your information immediately and provide you with exclusive services!

Back to Top