-

Whatsapp

+1 689 248 1956 -

Email

joannewong0817@gmail.com

14/01/2026

14/01/2026

In the real estate investment field, rental yield is a crucial indicator for measuring investment value. For investors seeking stable returns, identifying which U.S. cities offer the highest rental yields has become a focal point. From small towns in the Texas prairie region to small cities in New York State, and college towns in Florida, numerous investment opportunities with astonishing rental yields lurk across the United States. Texas, with its low housing prices and high rental yields, has become a highly sought-after destination for investors. Wichita Falls, a small town in the North Texas prairie region, boasts one of the highest rental yields in the nation thanks to its affordable housing prices and substantial rental returns. Here, a property valued at $84,000 can command a median rent of $938, resulting in a 13.4% return on investment. This high return is attributed to the local diversified economy; oil production and agriculture provide stable employment opportunities, while the nearby air force base generates a steady stream of rental demand. Lubbock, another Texas city, similarly attracts investors with its high rental yields. Lubbock, home to Texas Tech University and abundant oil and gas resources, boasts home prices at just $111,000, while the median rent reaches $1,089, resulting in an 11.8% return on investment. For investors seeking long-term, stable returns, Lubbock is undoubtedly an ideal choice. Turning our attention to New York State, Schenectady, another small city, is equally noteworthy. As the ninth largest city in New York, Schenectady offers home prices at just $153,000, while the median rent is a substantial $1,275, yielding a 10% return on investment. Tenants here are primarily students from Union College and employees of General Electric, providing investors with stable rental income. Gainesville, Florida, with its unique college town attributes, represents a high-yield rental market. Home to the…

14/01/2026

14/01/2026

In the wave of globalization, residency planning has become a crucial issue for many high-net-worth individuals and families. Real estate investment immigration, as an innovative model combining asset allocation and residency acquisition, is attracting increasing attention from investors. By purchasing property in specific countries, investors can not only achieve global asset allocation but also obtain permanent residency or citizenship for family members, opening new pathways for children’s education, career development, and improved quality of life. Europe, as the birthplace of real estate investment immigration policies, has seen several countries become popular choices due to their policy flexibility and welfare advantages. Greece’s “Golden Visa” program allows investors to apply for permanent residency for three generations of their family by purchasing property with a relatively low threshold. This policy not only eliminates complex requirements such as language and educational qualifications but also grants holders freedom to travel within the Schengen Area, provides children with a pure British education environment, and lowers the entry threshold for prestigious domestic universities through the Joint Entrance Examination for Overseas Chinese Students. Portugal’s real estate investment immigration policy is also highly favored. Investors who purchase property in core cities such as Lisbon and Porto can obtain a five-year residency permit with flexible renewal options and the ability to work and start a business. After five years, meeting residency requirements allows them to apply for citizenship and enjoy the full range of benefits of EU citizens. The Mediterranean island nation of Cyprus attracts business owners and investors with its status as a “tax haven.” Permanent residency can be obtained by purchasing real estate worth €300,000, with corporate income tax as low as 12.5%, and no inheritance or gift tax. Double taxation avoidance agreements with over 60 countries further reduce cross-border trade costs. For families with overseas businesses, Cypriot…

13/01/2026

13/01/2026

Many people think of attending an exhibition simply as: buy a ticket, go to the venue, and wander around. However, a truly good experience often comes from advance preparation. Whether you’re a general visitor, an industry professional, or a businessperson with purchasing or research purposes, good preparation saves time, avoids unnecessary detours, ensures you see truly valuable content, and helps you seize on-site offers and opportunities. Exhibitions are crowded and information-heavy; without a clear goal, it’s easy to get lost and confused. Without proper equipment, you risk exhaustion or missing key events. Lack of etiquette and communication skills can negatively impact subsequent networking. Preparation isn’t complicated; it mainly involves clearly listing the “essential items,” allocating your time and energy effectively, anticipating potential problems, and reserving solutions. Advance Registration and Confirmation of Participation Information Many exhibitions require online booking or real-name registration. Advance registration avoids queuing on-site. After registration, be sure to confirm your visit date, opening and closing times, time slots, and whether you have received your ticket/QR code. Pay attention to emails or official WeChat account notifications from the organizer, noting the exhibition hall address, entrance, and required identification (some exhibitions require ID cards or work permits). If the exhibition includes forums or breakout sessions, register for these activities in advance to secure your seat. Define your visiting objectives and create a must-see list Don’t just “see everything” on-site. First, clarify your objectives: To learn about industry trends? To find partners? To see new products? Or simply to broaden your horizons? Based on your objectives, create a “must-see list,” marking key booths, forums, and time slots. Prioritize items on the list, seeing the most important ones first, and adding the rest as time allows, avoiding a rushed visit. Plan your itinerary and routes Check the exhibition hall…

13/01/2026

13/01/2026

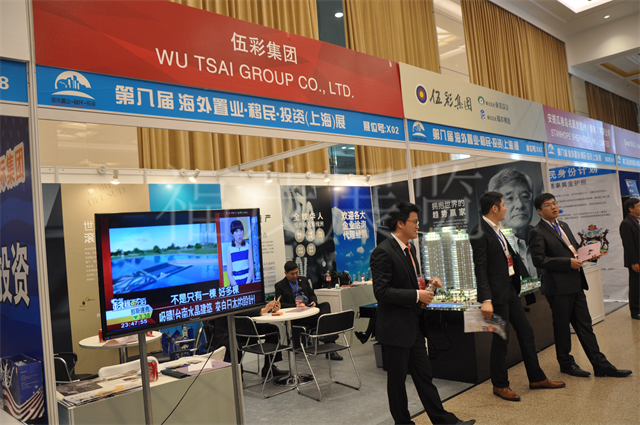

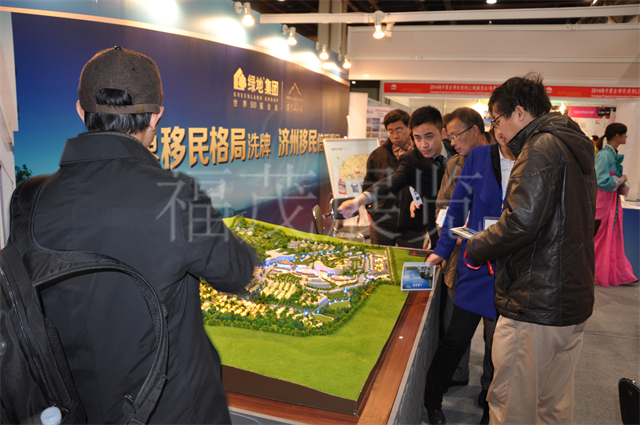

Attending a real estate expo is a shortcut for ordinary homebuyers, investors, and industry professionals to understand the market and a great opportunity to compare products and services. A good expo will present elements such as buying a house, viewing properties, financial services, policy consultation, interior design, and smart home technology, allowing you to see and compare all the information that would normally require visiting many places in one or several days. For ordinary people, visiting a real estate expo not only allows them to see new developments and model homes, but also provides on-site consultations on practical issues such as mortgages, taxes, floor plan modifications, and property management. For developers and real estate agents, it is an important window for launching new products, gathering clients, and closing deals. Exhibition Theme and Overall Layout Each expo will have a clear theme (e.g., residential, commercial, senior living, long-term rental apartments, or regional development), and the exhibition areas will be divided accordingly. The overall layout generally includes the developer exhibition area in the main exhibition hall, the theme exhibition area, the forum area, the experience area, and the supporting service area. First, checking the theme can help you quickly determine if the expo is relevant to your needs: is it primarily for upgrading your home, or focused on investment or commercial properties? New Property Showcase Area This is the most attractive part of the property expo. Developers will bring the latest property information, model rooms, floor plans, and renderings. Staff will be on-site to explain the property’s positioning, unit advantages and disadvantages, amenities, and sales policies. Viewing model rooms allows you to visually assess lighting, circulation, and decoration style, while the floor plan helps you understand the community layout and access points. Pre-owned and Exchange Area Many expos have dedicated…

13/01/2026

13/01/2026

Driven by the global popularization of higher education and the surge in demand for cross-border study abroad, overseas student accommodation is transforming from a niche investment into a new darling of the capital market. From smart apartments near the City of London to shared communities around the University of Sydney, these assets attract the attention of insurance funds, family offices, and individual investors due to their stable cash flow, counter-cyclical characteristics, and capital appreciation potential. However, behind their “stable” label lies a complex web of variables, including supply and demand dynamics, operational challenges, and regional differentiation. Investors need to see beyond the surface and find the answer in balancing returns and risks. The “stable” nature of student accommodation is primarily reflected in the resilience of rents supported by rigid demand. The commercialization of international education has driven the continuous growth in the number of international students worldwide. In English-speaking countries, for example, non-native students generally account for more than 20%, while university-owned accommodation coverage is less than 30%, directly creating a huge off-campus accommodation market. For instance, weekly rents for student accommodation in central London can reach over £350, with an average annual increase of 4%-6%, far exceeding the growth rate of ordinary residential rents. More importantly, students are less sensitive to rent and prioritize location and convenient amenities—apartments near subway stations, supermarkets, and libraries maintain occupancy rates above 95%, even with rents 10%-15% higher than market rates. This “rigid demand” allows student apartments to maintain stable returns during economic downturns, serving as a “safety net” for investors navigating economic cycles. Deep capital involvement further amplifies the investment value of student apartments. The accelerated deployment of private equity funds and REITs is upgrading the traditional “bedroom business” into an “experience economy.” Greystar, the largest student apartment operator in the US,…

13/01/2026

13/01/2026

Against the backdrop of growing global demand for asset allocation and residency planning, investment immigration has become an important pathway for many families to achieve multiple goals, including education, healthcare, and freedom of movement. However, immigration policies vary significantly across countries, with thresholds ranging from tens of thousands to millions of US dollars. Choosing the most cost-effective and manageable project is crucial. Considering the policies, costs, and application requirements of major global immigration countries, the following countries have become popular choices in the current investment immigration market due to their low thresholds, high flexibility, and clear legal support. Portugal is considered the “king of cost-effectiveness” for European immigration. Its investment immigration program, with a minimum investment of €500,000, is a preferred option for middle-class families seeking EU residency. Applicants need to invest in a government-approved fund, and the principal can be redeemed after 5 years. No long-term residency is required; only a 7-day stay per year is needed to meet the citizenship requirements. Even more attractive is the high value of the Portuguese passport, granting visa-free access to 187 countries, including major countries like the US and UK, and children can enjoy high-quality EU education resources. For families seeking “immigration without relocation,” Portugal’s relaxed policies and high degree of freedom are a perfect match. With budgets further reduced, the Greek real estate investment immigration program, which initially attracted many investors with its low threshold of €250,000, has seen prices rise to €500,000 in some areas, while others have maintained their original price. After purchasing property, the entire family can obtain a five-year residency permit, and the property can be rented out for stable income, with rental returns of approximately 4%-6%. Greek citizenship requirements are relatively lenient; applicants only need to hold property for seven years and pass a language test,…

13/01/2026

13/01/2026

For many families dreaming of overseas property investment, preparing the initial capital is often the first and most crucial step. Whether for children’s education, asset allocation, or immigration, the initial capital for overseas property purchase involves not only the price of the property itself but also covers taxes, agent fees, legal fees, and other expenses. So, how much initial capital is needed for overseas property purchase? This article will provide a detailed analysis from the perspectives of market characteristics, funding sources, and potential costs in different countries. The initial capital for overseas property purchase primarily depends on the property price level of the target country. Taking Southeast Asia as an example, the price of small apartments in the core area of Phnom Penh, Cambodia, is generally between $1,500 and $2,500 per square meter, with a 50-80 square meter apartment costing approximately $75,000 to $200,000. In Greece, the minimum investment threshold for “commercial-to-residential conversion” projects under the property investment immigration policy is €250,000, and permanent residency can be enjoyed for three generations of the family. In contrast, some regions of the United States’ EB-5 investment immigration program require an investment of at least $800,000 and additional conditions such as job creation. These data indicate that the initial capital required for overseas property purchases varies depending on the country, city, and project type, requiring precise allocation based on individual needs and budget. Besides the property price itself, sufficient funds must be allocated for taxes and fees when purchasing overseas property. For example, in Cambodia, foreign buyers must pay a 4% property transaction tax, along with additional expenses such as legal fees and agent fees, which typically account for 5% to 8% of the total property price. In Greece, property purchase immigration requires payment of property transfer tax, municipal tax, and legal fees,…

12/01/2026

12/01/2026

For many general visitors, attending trade shows is both novel and somewhat overwhelming. Trade shows are large-scale, crowded, and have densely packed booths. Without advance preparation, it’s easy to get tired halfway through, see a lot but remember nothing, or even miss truly interesting content. This is especially true for large-scale expos or industry exhibitions; after a day of walking around, not only are your legs sore, but you may also experience information overload. Actually, attending trade shows isn’t about “walking around as much as possible and seeing as much as possible,” but rather about visiting with a focus and pace. Even for general visitors, paying a little attention to key steps like registration and planning can significantly improve the experience. Register in Advance and Understand Entry Methods The first step in attending a trade show is often not arriving on-site, but registering in advance. Most trade shows now use online reservations or real-name registration, and some require obtaining e-tickets in advance. When registering, general visitors should pay attention to the opening hours, the date of their visit, and whether there are time slots for entry. Registering in advance not only avoids queuing on-site but also ensures you receive timely notifications and event schedules, providing a foundation for your subsequent planning. For popular exhibitions, the earlier you register, the better, to avoid limited spots closer to the opening date. Understand Exhibition Information and Clarify Your Visiting Purpose Before planning, take some time to understand the basics of the exhibition, such as its theme, main exhibition areas, and whether it’s geared towards professionals or the general public. Ordinary visitors don’t need to “see everything,” but rather to clarify what they most want to see: new products, technological experiences, or lifestyle displays. Having a general goal allows you to select key…

12/01/2026

12/01/2026

As a highly international city, Shanghai hosts various large-scale expos almost every year. Among these, the most attention-grabbing are often the comprehensive expos centered on international cooperation, trade exchange, and industry showcases. These expos are not only important platforms for companies to showcase their strengths and seek cooperation, but also increasingly become windows for the general public to understand cutting-edge technologies, international brands, and industry trends. For businesses, this is a great opportunity to expand markets and connect with resources; for visitors, it’s an experience of “seeing the world without leaving the country.” Many people are curious: What exactly is there to see at the Shanghai Expo? What are the highlights? Is it worth attending? High Internationalization and Wide Scope of Exhibitors One of the biggest highlights of the Shanghai Expo is its high level of internationalization. Companies, institutions, and brands from different countries and regions gather together, covering multiple fields such as manufacturing, services, technology, consumer goods, and cultural creativity. This diversified exhibitor structure makes the expo not only about “seeing products” but also about “seeing trends.” Whether it’s international brands or distinctive companies from emerging markets, they can all showcase their advantages on the same platform, providing visitors with a broader perspective. Exhibits Closely Connected to Daily Life, Strong Experiential Engagement Unlike traditional exhibitions that are “look but don’t touch,” the Shanghai Expo increasingly emphasizes interaction and experience. Many exhibition areas use physical displays, live demonstrations, and interactive experiences to allow visitors to intuitively experience products and technologies. From daily consumer goods to smart devices, from healthy living to green environmental protection, exhibits are often closely related to daily life, not lofty concepts, but things that “might be useful in the future,” which is a major reason for attracting a large number of ordinary visitors. Cutting-Edge…

12/01/2026

12/01/2026

High school graduation is a significant turning point in life. For many students, studying abroad is both an opportunity to broaden their horizons and a strategic investment in their future career development. However, with hundreds of countries and thousands of universities to choose from, how to plan a path that aligns with personal interests and maximizes the value of studying abroad has become a shared concern for students and parents. From language preparation to university selection, from application strategies to resource integration, every step requires precise planning to ensure a smoother and more successful study abroad journey. Language proficiency is a fundamental requirement for studying abroad, but the methods for improvement must be tailored to the individual. For English-speaking countries, IELTS or TOEFL scores are core application requirements, but simply “scoring high” is not the only goal. Many students find themselves stuck in a cycle of repeated testing with stagnant scores, stemming from a lack of real-world language experience. It is recommended to start in high school by participating in international exchange programs, joining English debate clubs, or watching English films and television shows without subtitles to cultivate comprehensive listening, speaking, reading, and writing skills. For non-English-speaking countries, such as Germany, France, or Japan, learning the target language in advance not only enhances application competitiveness but also clears obstacles for future studies and life. For example, German universities generally require a German language proficiency level of C1, while some prestigious Japanese universities have specific requirements for N1 scores. The adequacy of language preparation directly impacts admission results. The choice of universities and majors needs to balance interests and career orientation. Some students blindly pursue the “prestige of prestigious universities” while neglecting the suitability of their chosen major, leading to insufficient motivation after enrollment or employment difficulties after graduation. The correct…

12/01/2026

12/01/2026

For many families, overseas property purchases are not only an asset allocation choice but also a long-term plan for their children’s education and retirement. However, unlike the simple “one-time payment” model of domestic property purchases, overseas property purchases involve a full-cycle tax system from transaction to holding, and even slight missteps can significantly reduce investment returns. Understanding the differences in taxation across countries has become an “invisible hurdle” that overseas property buyers must overcome. Tax differences during the property purchase stage are often reflected in the transaction process. In the UK, for example, stamp duty is the first hurdle buyers must face: no stamp duty is required for properties valued below £125,000, while the excess is taxed at a tiered rate, reaching a maximum of 12%. This “higher price, higher tax” design directly increases the transaction costs of high-end properties. In Australia, different states have different stamp duty rates. New South Wales typically charges 4%-5%, with an additional 8% surcharge for overseas buyers, further increasing the cost of purchasing property for non-residents. It’s worth noting that some countries lower the threshold through preferential policies. For example, Cyprus exempts overseas buyers of properties worth over €300,000 from VAT and directly grants them permanent residency. This “tax-for-status” model has attracted a large number of immigrant investors. However, the tax burden during the holding period is more persistent. The US property tax mechanism is a typical example: tax rates vary from 0.2% to 3% across states, with some areas in New Jersey exceeding 2%. A $500,000 property would incur over $10,000 in property taxes annually. This characteristic of “the higher the property price, the heavier the tax burden” forces investors to carefully assess the balance between rental income and holding costs. Canada, on the other hand, uses a “vacancy tax” to incentivize efficient…

12/01/2026

12/01/2026

With the increasing demand for global asset allocation, overseas real estate investment has become an important choice for many investors to expand their wealth portfolios due to its advantages such as risk diversification and stable returns. However, cross-border investment involves different legal systems, economic environments, and cultural differences between countries. First-time investors, lacking systematic planning, are prone to falling into the trap of information asymmetry or decision-making biases. From target positioning to risk management, each step requires careful consideration to achieve steady asset appreciation. Clearly defining investment objectives is the primary task in overseas real estate investment. The characteristics of real estate markets vary significantly across different regions, and investors need to choose a suitable direction based on their own needs. If seeking rental returns, priority should be given to cities with stable population inflows and strong rental demand, such as the capital cities of some Southeast Asian countries, where the concentration of young people and the increase in foreign workers have led to an active long-term rental market and consistently low vacancy rates. If focusing on asset appreciation, attention should be paid to areas benefiting from infrastructure development in emerging economies, such as newly developed areas in some cities. With the extension of rail transit or the improvement of commercial facilities, property prices often show a rapid upward trend. Furthermore, the demand for education-related immigration has given rise to the concept of “school district housing.” Some countries allow residency through property purchase, but it’s crucial to verify policy details to avoid investment losses due to misunderstandings. In-depth market research is a key step in mitigating risk. Significant information gaps exist in overseas real estate markets, and relying solely on “average price” data provided by agents can easily lead to misjudgments. Investors need to analyze multiple dimensions to uncover the…

Number

NumberCall Now:

139 1723 4508

WeChat

WeChat

Form

FormBook Your Booth

Complete your information immediately and provide you with exclusive services!

Back to Top