-

Whatsapp

+1 689 248 1956 -

Email

joannewong0817@gmail.com

04/02/2026

04/02/2026

Do you dream of owning property overseas, hoping to create a warm haven in a foreign land, or to increase your wealth through real estate investment? However, the path to overseas property purchase is not smooth sailing; many pitfalls lurk, and a moment’s carelessness can shatter your dreams and cause financial losses. Today, we’ll expose the true nature of ten common pitfalls in overseas property purchases. Initial Information Gathering False Property Information:Some agents or developers exaggerate or even fabricate property advantages to attract buyers, such as claiming the imminent completion of a large commercial center nearby or the property boasting stunning sea views, but these are often untrue. Unfamiliarity with Market Rules:Real estate market rules vary greatly from country to country, encompassing purchase procedures, tax policies, and property types. For example, some countries require high property taxes and stamp duties, and property rights may be divided into freehold, leasehold, and other forms. Buyers unfamiliar with these rules are easily put at a disadvantage. Ignoring Exchange Rate Fluctuation Risks:Overseas property purchases involve the exchange of different currencies, and exchange rate fluctuations can significantly impact purchase costs and future returns. Failure to fully consider exchange rate factors when purchasing a property may result in losses during payment or subsequent resale. During the Home Purchase Transaction Contract Clause Traps: Contract clauses may be vague or lack clear responsibilities. For example, the stipulations regarding property delivery standards and liability for breach of contract may be insufficiently detailed, making it difficult for buyers to protect their rights should problems arise. Underhanded Agent Practices: Some unscrupulous agents collude with developers to inflate prices and profit from the difference, or conceal the true condition of the property, such as legal disputes or quality issues. Unclear Property Rights: The purchased property may have ownership disputes, such as…

02/02/2026

02/02/2026

In the wave of global asset allocation, overseas real estate investment has become an important path for many to achieve wealth appreciation and lifestyle upgrades. From Southeast Asian beachfront apartments to villas in ancient European cities, the unique value of different markets attracts more and more investors to step out of their comfort zones. However, practical challenges such as language barriers, legal differences, and cultural gaps deter many newcomers. How to systematically plan your first overseas investment? Mastering the following core strategies will help investors find a balance between opportunities and risks. Define Investment Objectives: A Compass for Direction The motivations for overseas real estate investment are diverse, and it is necessary to clearly define the core objectives before starting. If seeking long-term rental income, priority should be given to cities with net population inflows and active job markets, such as school district properties in Melbourne, Australia, or properties near technology parks in Berlin, Germany. If focusing on asset preservation, attention can be paid to prime locations in politically stable and legally sound developed countries, such as detached houses in Vancouver, Canada, or vacation villas on the shores of Lake Geneva, Switzerland. If planning for children’s education, it is necessary to focus on school resources and the living environment; properties near Harrow School in London, UK, or government-subsidized housing in Singapore are typical examples. Once the target is clearly defined, the investment scope and risk tolerance will naturally become clear, avoiding decision-making interference from short-term market fluctuations. Target Market Selection: Data-Driven Decision-Making Model Global real estate markets vary significantly, requiring a multi-dimensional indicator-based selection framework. Economic fundamentals are paramount: GDP growth, unemployment rates, and population structure reflect market potential. For example, Portugal’s “Golden Visa” policy attracts a large influx of European immigrants, leading to continuously rising demand for Lisbon…

30/01/2026

30/01/2026

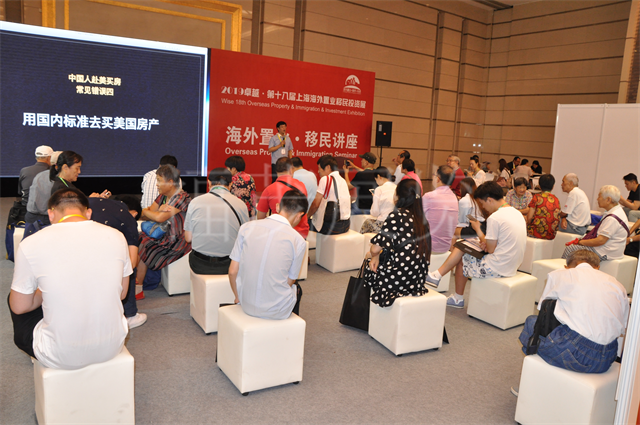

With increasingly interconnected global economies, overseas real estate investment is gaining wider attention. More and more investors are focusing on real estate markets in different countries and regions, hoping to diversify their asset allocation, upgrade their living needs, or achieve long-term stable returns through overseas property investment. However, the fragmented nature of overseas real estate market information, complex policies, and significant language and cultural differences present considerable challenges for investors in understanding and making informed judgments. Against this backdrop, overseas real estate expos have emerged and are gradually becoming important platforms for understanding global real estate investment. The biggest features of overseas real estate expos are their “centralization” and “efficiency.” Real estate developers, intermediaries, and related service providers from multiple countries and regions gather together, presenting investors with information that was previously scattered across various markets. Whether you are a newcomer just starting to explore overseas real estate or an experienced investor, you can quickly learn about market conditions, project types, and investment methods in different countries at the expo. This one-stop information access method significantly reduces the learning and time costs associated with overseas real estate investment. Centralized Presentation of the Global Market The most prominent advantage of overseas real estate expos is their centralized display of global real estate market information. At the expo, investors can simultaneously access real estate projects from multiple regions across the Americas, Europe, and Asia, encompassing various types including residential, commercial, and vacation properties. This concentrated presentation allows investors to quickly gain a comprehensive understanding of the global real estate market. Through on-site demonstrations and explanations, investors can learn about price levels, investment thresholds, purchase processes, and holding costs in different countries. Compared to piecemeal research or individual consultations, this systematic approach to information acquisition is more intuitive and facilitates clearer judgments….

30/01/2026

30/01/2026

Driven by globalization, overseas real estate investment has gradually become an important part of asset allocation for many investors. Whether pursuing asset diversification or seeking higher investment returns, overseas real estate seems to exude an alluring glow. Various real estate-related exhibitions and events occasionally build bridges for investors to access overseas property projects, showcasing the vibrant overseas real estate market. However, behind this glamorous facade, are there hidden risks? Is overseas real estate a safe haven for investment, or a whirlpool of hidden risks? What makes overseas real estate investment so attractive? The primary reason for the popularity of overseas real estate investment lies in its potential for appreciation. In regions with rapid economic development and continuous population growth, the real estate market often exhibits strong growth momentum. For example, in some emerging markets in Southeast Asia, with the continuous improvement of infrastructure and the influx of foreign capital, housing prices and rental levels have continued to rise, bringing considerable returns to investors. At some real estate exhibitions, projects in these popular regions often become the focus, attracting the attention of many investors and giving them hope for wealth growth. Furthermore, overseas real estate investment can help investors diversify their assets and mitigate the risks brought by fluctuations in the domestic market. When the domestic real estate market experiences adjustments, the stable performance of overseas markets may offer investors a sense of security. By participating in relevant exhibitions, investors can access real estate projects from around the world in one place, easily achieving cross-regional asset allocation and broadening their investment horizons. The risks of overseas real estate investment cannot be ignored However, overseas real estate investment is not without its challenges, and numerous risks lurk beneath the surface. Policy risk is one of the most significant. Real estate…

29/01/2026

29/01/2026

In the global asset allocation wave, the US real estate market has become a focal point for overseas investors due to its stable market environment, transparent legal system, and diversified investment options. Whether you are a conservative investor seeking long-term rental income or an aggressive buyer aiming for property appreciation, the US market offers suitable targets. However, cross-border investment involves multiple challenges, including capital flows, tax planning, and legal compliance, making systematic planning crucial. This article will analyze the market from four dimensions: market selection, capital flow, legal compliance, and risk management, providing investors with a practical operational guide. Precise Positioning: Choosing the Right Market and Targets The US is vast, and the characteristics of real estate markets vary significantly across different regions. Investors need to select core areas based on their own goals and risk appetite. For example, first-tier cities like New York and San Francisco have strong economic vitality and continuous population inflows, resulting in resilient property prices, but the investment threshold is high, making them suitable for long-term holders with ample funds. Emerging cities like Austin, Texas, and Tampa, Florida, have seen significant price increases due to industrial upgrading and population migration, and rental yields are generally higher than the national average, making them suitable for investors seeking appreciation potential. Furthermore, the choice of property type is equally important—detached houses are suitable for suburban areas with high family rental demand, apartments are better suited to young renters in urban core areas, and commercial real estate (such as warehousing and logistics) requires attention to regional industrial planning and logistics network layout. Funding Path: Establishing Cross-Border Payment and Financing Channels One of the core challenges of overseas investment is the cross-border flow of funds. Investors need to plan their funding sources and payment methods in advance to avoid…

28/01/2026

28/01/2026

As traditional immigration channels gradually close due to tightening policies, an innovative “property-for-citizenship” model is sweeping the globe—obtaining Golden Visas through real estate investment. From sea-view properties in Greece along the Mediterranean coast to holiday villas in the Caribbean, savvy investors have discovered that purchasing overseas property not only yields asset appreciation but also unlocks multiple benefits such as residency rights, educational opportunities, and tax advantages. This “killing multiple birds with one stone” strategy is reshaping the global asset allocation logic of high-net-worth individuals. Policy Dividends: How Countries Attract Global Capital Through Real Estate Europe has become the main battleground for this transformation. Portugal pioneered the “Golden Residence Permit Program,” allowing investors to obtain residency by purchasing real estate worth €500,000. This model was quickly imitated by countries such as Spain and Greece. Greece further lowered the threshold to €250,000, launching a “€250,000 property purchase for three generations of the family to immigrate” policy, directly igniting market enthusiasm. These projects generally allow property rentals, allowing investors to enjoy an average annual rental return of 4%-6% while obtaining residency. The Caribbean region, however, has taken a different approach. St. Kitts and Nevis has launched a “real estate + citizenship” package, allowing investors who purchase real estate worth over US$400,000 to resell it after five years while retaining their citizenship. This “identity assetization” design makes real estate a tradable “hard currency.” Antigua and Barbuda has innovatively introduced a “National Development Fund + Real Estate” dual option to cater to different investment preferences. Emerging Asian markets are also keeping pace. Malaysia’s “My Second Home” program, while not strictly a golden visa, grants a 10-year renewable residency permit by purchasing real estate worth over RM500,000. This “quasi-immigration” policy has attracted a large influx of retirees and remote workers to tourist destinations like…

27/01/2026

27/01/2026

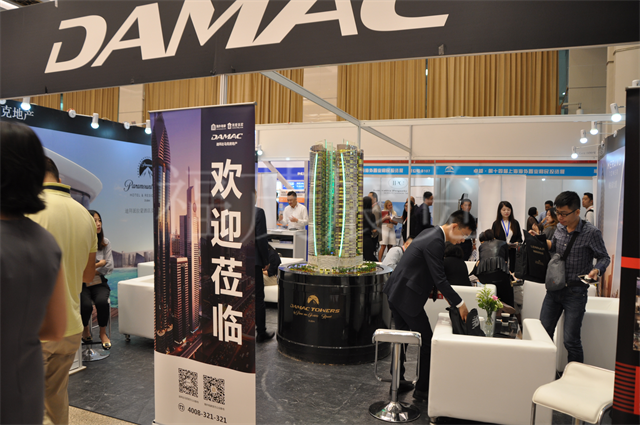

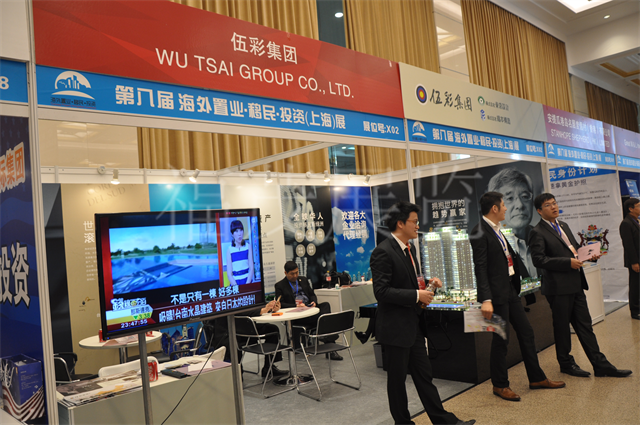

In the context of increasing global economic integration, overseas real estate has gradually become an important area of focus for many investors, practitioners, and related institutions. Overseas real estate expos have emerged in this environment and have gradually developed into an important platform integrating information exchange, project display, cooperation negotiation, and resource matching. For individual investors, expos are a window to understanding overseas markets; for real estate companies and agencies, expos are an important channel to expand clients, build brands, and find partners. Therefore, participating in overseas real estate expos is not merely “visiting” or “exhibiting,” but has multiple practical significance and value. Many people’s understanding of overseas real estate expos is still limited to “looking at projects” and “listening to introductions,” believing it’s simply about obtaining project information. However, the core value of expos goes far beyond this. They provide a highly concentrated information environment and exchange scenario, allowing exhibitors to access real estate market information from multiple countries and regions in a short period, understanding different types of projects, policy backgrounds, and market demands. At the same time, through face-to-face communication, exhibitors can more intuitively judge project quality and the professionalism of potential partners—an experience that is difficult to replace through online channels. Centralized Market Information Acquisition The most direct and fundamental value of overseas real estate expos lies in their highly centralized information. Normally, understanding the real estate markets of multiple countries requires consulting numerous documents and communicating with different organizations, which is time-consuming and laborious. However, at an expo, developers, agents, and service providers from different countries and regions showcase their projects, allowing attendees to compare and understand multiple markets simultaneously in one place. This centralized information acquisition method helps attendees quickly build a comprehensive understanding of overseas real estate markets. For example, price levels,…

26/01/2026

26/01/2026

With the acceleration of globalization, more and more investors are focusing on overseas real estate markets, seeking greater opportunities and returns. From Europe and America to Asia and Latin America, the potential and development trends of global real estate markets vary, but some regions have become popular destinations for investors due to their unique geographical, economic, or policy advantages. When choosing to invest in overseas real estate, in addition to considering factors such as the local economic situation, population structure, and policy environment, investors also need to pay attention to market stability, future appreciation potential, and policy support. With the improvement of people’s living standards and the diversification of global investment markets, overseas real estate markets are no longer the exclusive domain of a few wealthy individuals. More and more small and medium-sized investors also hope to achieve asset appreciation through cross-border investment. Especially against the backdrop of low interest rates and long-term appreciation, overseas real estate markets have become an important channel for capital preservation and appreciation. Through the analysis of popular overseas investment regions, we can see the differences in investment value, rate of return, and risks among different countries and regions. Within these regions, the real estate markets of some countries have been driven by multiple factors such as policy, economy, and culture, attracting a large influx of international capital. A Market Offering Stability and Returns The United States, as one of the world’s largest and most mature real estate markets, remains a top destination for overseas investors. The US real estate market is broad, offering diverse investment opportunities from major metropolitan areas like New York and Los Angeles to secondary cities like Texas and Florida. The advantages of the US real estate market lie in its large size, transparent legal environment, and relatively stable…

26/01/2026

26/01/2026

In recent years, overseas real estate markets have attracted increasing attention from investors. With globalization and the growing demand for diversified asset allocation, more and more Chinese investors are participating in overseas real estate markets. Overseas real estate expos have become an important platform for showcasing and exchanging information, helping investors understand the latest market dynamics and providing them with a wealth of choices. Through an analysis of several recent overseas real estate expos, we can see which countries and regions have become popular choices for investors. With China’s economic growth and the improvement of people’s living standards, more and more people are seeking ways to diversify their assets and preserve and increase their capital. Overseas real estate, especially in developed countries in Europe, America, and Asia, has gradually become the first choice for investors. By participating in overseas real estate expos, investors can obtain real-time market information, understand policy changes, market trends, and investment risks in different countries, thereby making more accurate investment decisions.Next, we will analyze the current hot spots in overseas real estate markets from several major countries and regions. A detailed market analysis will help investors better understand which countries are most popular and why they attract a large amount of foreign investment. United States: A Stable Investment Paradise The US real estate market has long been a popular choice for overseas investors, especially among Chinese investors, where the US has always held a significant position. The US real estate market boasts a relatively stable investment environment, especially in major cities like New York, Los Angeles, San Francisco, and Miami, which have consistently been key areas of focus for investors. The advantages of the US real estate market are primarily reflected in its transparent legal system and stable economic environment. The US has…

26/01/2026

26/01/2026

In the global asset allocation wave, overseas real estate investment, due to its characteristics such as inflation protection and stable returns, has become an important choice for high-net-worth individuals to diversify risk. From Mediterranean holiday apartments to promising new towns in Southeast Asia, the market characteristics of different countries are attracting investors with specific needs. This article will provide an in-depth analysis of the most popular overseas real estate investment destinations, revealing their core appeal and potential risks. Greece: Golden Visa Fuels Holiday Real Estate Boom As a benchmark for European tourism real estate, Greece continues to attract global investors with its “€250,000 real estate investment immigration” policy. Small apartments in areas such as Crete and the Ionian Islands have become new investment favorites, with 60-70 square meter two-bedroom projects becoming popular choices on short-term rental platforms due to stable rental returns and high resale liquidity. More notably, the Greek government allows real estate investments of HKD 50 million or more to be included in the immigration asset category. This dual allocation model of “residency + assets” is attracting more and more Asian investors. Portugal: A Blend of Cultural Heritage and Policy Advantages Historic cities like Lisbon and Porto not only boast World Heritage sites but are also popular destinations for European immigrants due to their “Golden Visa” policy. Investors can obtain residency by purchasing property worth €500,000, and can freely dispose of the property after five years. Market data shows that high-end residential prices in Portugal have risen by over 30% compared to previous years. Buyers from the Netherlands and Germany tend to choose well-equipped holiday villas, while short-term investors focus on apartment projects in emerging areas like Coimbra, where rental yields are generally higher than in the capital region. Australia: A Stable Market and Demand for…

24/01/2026

24/01/2026

The real estate market is influenced by multiple factors, including the economic environment, policy regulations, consumer demand, and market supply. In today’s globalized and information-driven world, overseas real estate exhibitions have become an important platform for understanding and grasping market dynamics. Through these exhibitions, exhibitors can not only access the latest market information but also engage in in-depth exchanges with industry experts, developers, and investors, gaining valuable market insights. The Role of Exhibitions Overseas real estate exhibitions are important exchange platforms for the global real estate industry. By participating, industry professionals can obtain firsthand market information, industry trends, and policy changes. The scale and influence of the exhibition directly affect the exhibitors’ gains. Generally, exhibitions are divided into local and international exhibitions, with the latter providing more resources and information from cross-border markets. Exhibitors can learn about the market strategies and development trends of companies or investors from different countries by exchanging ideas. Furthermore, exhibitions provide exhibitors with an opportunity to showcase themselves and expand their networks. For real estate developers, investors, and sales companies, exhibitions are not only a platform to showcase projects but also an opportunity to attract potential clients and partners. By interacting with participants from diverse backgrounds, one can gain a comprehensive understanding of changes in the global real estate market, enabling more forward-looking decision-making. How to Understand Market Dynamics Through Trade Shows? Focus on the Trade Show Theme and Participants Each trade show typically has a central theme, revolving around current market hotspots. Exhibitors can learn about the trade show’s focus areas from promotional materials, lecture topics, and the backgrounds of exhibitors. For example, some trade shows may focus on the residential real estate market, while others may emphasize commercial real estate or green building. Understanding the main content of the trade…

24/01/2026

24/01/2026

Imagine owning a property in a foreign country, enjoying rental income while passively waiting for asset appreciation, and even achieving a “property-for-property” wealth cycle through clever management—this is not an unattainable dream. With the acceleration of globalization, overseas real estate investment has become an important asset allocation option for high-net-worth individuals. However, the returns on real estate vary significantly across different countries, cities, and even neighborhoods. How can investors avoid the “inefficiency trap” and accurately target high-return projects? This article will reveal the “golden code” to high-return overseas real estate for investors, covering market selection, strategy formulation, and risk management. Core Cities: The “Ballast” for Stable Returns Core cities with strong economic vitality are often “safe zones” for overseas real estate investment. These areas have dense populations, abundant job opportunities, strong rental demand, and significant potential for property appreciation. For example, in London, small apartments around the City of London consistently offer rental yields of 4%-6% due to convenient transportation and comprehensive amenities, with extremely low vacancy rates. Even during periods of economic volatility, properties in prime locations maintain their resilience due to their “scarcity.” Take Austin, USA, for example. As a rising star in the tech industry, the arrival of giants like Amazon and Tesla has led to a surge in population and sustained strong housing demand. Apartment rents in the area have increased by 5%-8% annually, while property prices have risen even faster, creating a dual-income model of “rent + appreciation.” The investment logic for real estate in core cities is simple and direct: choose areas with high employment density and net population inflow, and hold long-term to enjoy the city’s development dividends. Emerging Areas: Potential “Dark Horse Tracks” For those seeking higher returns, emerging areas often harbor “hidden champions.” These areas typically experience rapid population…

Number

NumberCall Now:

139 1723 4508

WeChat

WeChat

Form

FormBook Your Booth

Complete your information immediately and provide you with exclusive services!

Back to Top