-

Whatsapp

+1 689 248 1956 -

Email

joannewong0817@gmail.com

25/12/2025

25/12/2025

For first-time homebuyers in Australia, the process is both the starting point for realizing their dream of homeownership and a complex journey involving financial planning, market insight, and legal compliance. The Australian property market is constantly evolving due to factors such as population growth, housing supply and demand, and economic cycles. Against this backdrop, first-time buyers need to grasp market dynamics and develop precise strategies tailored to their own needs to achieve their “homeownership dream” in a highly competitive market. Budget planning is the cornerstone of the homebuying process, and its complexity is often underestimated. For example, for an AUD 800,000 apartment in Sydney, the down payment is typically 10%-20% of the property price, or AUD 80,000 to AUD 160,000, but the actual expenses are much higher. In addition to the down payment, approximately AUD 32,000 needs to be allocated for stamp duty (calculated at 4%), AUD 5,000 for legal fees, AUD 2,000 for building inspection fees, and annual expenses such as property management fees and council fees. For overseas buyers, an additional 8% stamp duty surcharge and a 4% land tax surcharge are also required. Therefore, it is recommended that homebuyers set their total budget at 130%-150% of the property price and optimize their financial structure through government subsidies (such as the First Home Buyer Grant), savings, or parental property guarantees. For example, the New South Wales government offers subsidies of up to AUD 10,000 for first homebuyers, and stamp duty is waived for new homes under AUD 600,000. These policies should be included in budget planning in advance to avoid missing out on desired properties due to funding gaps. Loan strategies should balance flexibility and risk control. Pre-approval of a loan is crucial in the homebuying process. Applying for pre-approval through a mortgage broker or bank clarifies one’s…

24/12/2025

24/12/2025

In the United States, homeownership insurance is a core element in protecting assets. Whether it’s a mandatory requirement for mortgage purchases or a way to hedge the risks of cash purchases, choosing the right type of insurance and strategy directly impacts the stability of family finances. However, the US homeownership insurance system is complex, encompassing various types from basic fire insurance to comprehensive liability insurance, and with significant differences in state laws and natural environments. This article will provide homebuyers with a systematic guide from three dimensions: insurance type analysis, core selection strategies, and regional risk management. The core types of US homeownership insurance are framed by the HO (Homeowner) policy, covering different living scenarios and risk needs. HO-1, as the most basic “fire insurance,” only covers 10 specified disasters such as fire and lightning strikes, offering limited coverage and is often used for older homes or as the minimum requirement for mortgages. HO-2 expands upon HO-1 to cover 16 risks, including common issues like frozen pipes and heavy snowfall, suitable for families with limited budgets who need basic protection. HO-3 is the mainstream choice in the market, employing an “open-ended risk” clause. Except for explicitly excluded events like war and earthquakes, it covers almost all structural damage to the house, and includes liability and medical expense coverage to address scenarios such as visitor accidents and pet injuries. For high-value properties or collectors, HO-5 offers more comprehensive personal property protection, also employing an open-ended risk clause, and has higher payout limits for valuables such as jewelry and artwork. Apartment owners should choose HO-6, which focuses on interior structural damage (such as walls and floors) and personal property, while also covering liability for incidents in common areas. However, it’s important to ensure proper integration with the Owners Association (HOA) main policy…

23/12/2025

23/12/2025

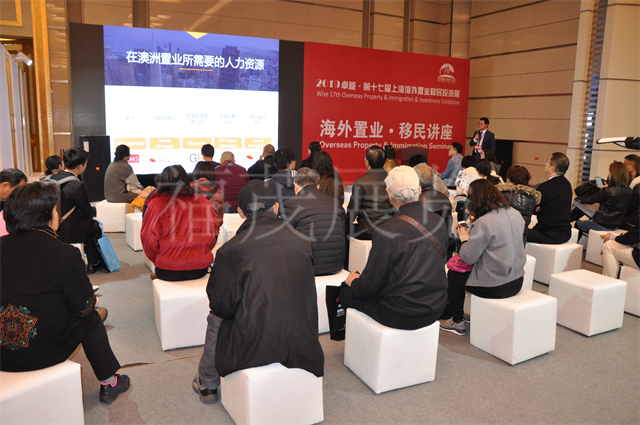

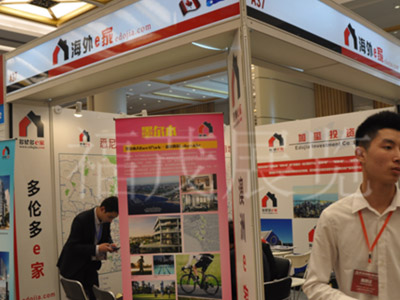

Against the backdrop of a increasingly differentiated global real estate market and more rational investor decisions, real estate developers are facing the real challenges of rising customer acquisition costs and greater difficulty in brand communication. Especially when targeting cross-border homebuyers and international investors, single-channel promotion is no longer sufficient to meet developers’ dual requirements of efficiency and precision. In this market environment, the value of professional real estate expos is becoming increasingly apparent. Real estate expos are no longer just simple project display venues, but efficient platforms integrating brand exposure, customer matching, resource integration, and trend insights. For overseas real estate developers, leveraging established exhibition platforms to enter target markets can significantly shorten the market cultivation cycle and improve project reach efficiency. The 2026 Wise Shanghai Overseas Property, Immigration, and Study Abroad Exhibition serves as an important bridge connecting developers with high-quality homebuyers. Concentrated Reach of Highly Matched Target Customers One of the biggest advantages of real estate expos is their ability to reach a large number of potential customers with clear purchasing intentions and investment needs in a short period of time. Compared to scattered promotion, the audience gathered at expos often already possesses a certain level of awareness and decision-making intent. For developers, this high-density, highly relevant customer environment helps improve communication efficiency and reduce ineffective promotion. Through on-site interactions, developers can directly understand customer concerns, tailor project advantages, and lay the foundation for future conversions. Rapidly Enhance Brand Exposure and Market Awareness In cross-border real estate transactions, brand awareness is a crucial prerequisite for building trust. Real estate expos provide developers with a centralized window to showcase their brand image. Through unified booth design, professional presentations, and continuous on-site exposure, developers can quickly increase brand visibility. Compared to the fragmented dissemination of online promotion, the brand…

23/12/2025

23/12/2025

Against the backdrop of continuously rising global asset allocation and cross-border investment demand, overseas real estate developers are ushering in new development opportunities. An increasing number of high-net-worth individuals, families, and institutional investors from China and other Asian markets view overseas real estate as an important option for asset preservation, risk diversification, residency planning, and long-term returns. However, while market demand is growing, competition is also intensifying. How to effectively expand business in an environment of high information transparency and increasingly rational customer decision-making has become a core issue that overseas real estate developers must address. For developers, relying solely on traditional channels or price advantages is no longer sufficient to form long-term competitiveness; a systematic approach is needed across multiple dimensions, including brand building, channel development, customer awareness, and service systems. Especially in cross-border transactions, cultural differences, policy understanding, trust building, and service depth often directly impact transaction efficiency and brand reputation. The 2026 Wise Shanghai Overseas Property, Immigration, and Study Abroad Exhibition will provide overseas real estate developers with an important window for direct dialogue with target customers. Defining Target Markets and Customer Positioning The first step for overseas real estate developers in expanding their business is to clearly define their target markets and core customer groups. Housing demand varies significantly across different countries and regions. Some prioritize asset allocation, others focus on owner-occupancy, while still others are closely tied to education and residency planning. Developers need to accurately match potential customer profiles based on their project type, price range, and location attributes. Simultaneously, they should avoid a “broad-based” promotional strategy and instead focus on in-depth outreach to highly relevant demographics. Clear market positioning not only improves marketing efficiency but also fosters stronger brand recognition among customers, laying the foundation for future conversions. Building a Trustworthy Brand…

23/12/2025

23/12/2025

Amid the global asset allocation trend, overseas property purchases have become a crucial risk diversification option for high-net-worth individuals. However, loan policies vary significantly across countries. From down payment ratios and interest rate fluctuations to loan terms and approval conditions, each rule directly impacts the cost and feasibility of purchasing a property. This article will provide an in-depth analysis of loan ratio policies in major overseas property markets such as the US, UK, Japan, Singapore, and Australia, offering precise decision-making support for homebuyers. The US market exhibits a dual characteristic of “coexistence of lenient and stringent” policies. As the world’s most liquid real estate market, the US does not restrict the number of properties owned by overseas buyers, but its loan policies clearly differentiate between local and foreign buyers. Local buyers can apply for loans up to 90% of the property value, while overseas buyers typically face a 60% loan cap, and loans are almost never accepted for properties under $300,000. This difference stems from banks’ considerations regarding the risk of cross-border asset recovery. It is worth noting that the Federal Reserve’s continued interest rate cuts since 2025 have pushed mortgage rates down from 7% to below 6%, with 15-year loans potentially even dropping to 5.5%, saving homebuyers substantial interest expenses. For example, with a $500,000 property and a 60% loan-to-value ratio, overseas buyers would need a $200,000 down payment. If the interest rate drops from 7% to 6%, the total interest expense over a 30-year repayment period could be reduced by approximately $120,000. The UK market attracts global investors with its “high leverage and low interest rates.” As a global financial center, London treats overseas buyers and local residents equally in its lending policies, allowing for loan-to-value ratios of up to 70%, with some banks even offering products with…

22/12/2025

22/12/2025

In the UK, school district housing is not only a stepping stone for families to secure quality education for their children, but also a focal point for global investors due to its scarcity and long-term appreciation potential. As competition for educational resources intensifies in core cities like London, the supply-demand imbalance for school district housing has become increasingly prominent, leading to a continuous rise in property prices. This article will analyze the core value and investment strategies of school district housing, based on the latest market dynamics in London and surrounding areas, providing practical reference for families and investors. London, as the city with the highest concentration of educational resources in the UK, exhibits a clear regional differentiation in its school district housing market. Taking Barnet as an example, as the largest borough in London, the area boasts 117 schools, 91% of which have received an “Outstanding” or “Excellent” rating in the Ofsted assessment, including the top-ranked state grammar school, Queen Elizabeth’s School. Benefiting from the dual advantages of high-quality educational resources and a livable environment, Barnet’s property prices have steadily increased in recent years, making it a top choice for middle-class families. Similarly, Richmond, with its historical landmarks like Hampton Court Palace and top-tier public and private schools, has consistently ranked first in the UK’s Happiness Index for many years. Its detached properties command high prices due to high demand, attracting high-net-worth individuals worldwide. For families with limited budgets, there are also cost-effective options in the outer suburbs of London. Kingston, one of London’s four Royal Boroughs, is renowned for its exceptionally high percentage of primary and secondary schools, with 24 out of 34 rated “Outstanding.” Tiffin Girls’ School and Tiffin School, in particular, have a 25% student admission rate to Oxford and Cambridge each year. Average house prices…

20/12/2025

20/12/2025

For many attendees, overseas property trade shows are often an information-dense experience: encountering multiple countries, cities, and projects in a short period, and hearing a plethora of introductions about “potential,” “planning,” and “opportunities.” However, what truly differentiates investors is not the amount of information acquired, but rather the ability to discern information and filter directions. At trade shows, passively receiving project presentations can easily lead to being attracted by appearances while neglecting the crucial long-term risk boundaries in real estate investment.In the current context of a more complex global environment and increasingly rational overseas investment, how to efficiently determine whether an overseas property is worth further investigation at a trade show has become a question every attendee needs to consider. The 2026 Wise Shanghai Overseas Property, Immigration & Study Abroad Exhibition (March 29-31, 2026) is not only a platform to understand projects but also a vital opportunity to establish an investment judgment framework. What is the long-term development direction of this country and city? At trade shows, the first step in judging overseas property is never to look at the project itself, but to understand the long-term development logic of the country and city. Real estate cannot exist independently of cities and nations. Even the most exquisite projects will struggle to maintain long-term value if the region lacks long-term development support. This question helps understand a city’s role in the overall national development and its ability to continuously attract resources and population. Who are the main buyers of local real estate demand? The core of real estate is demand structure, not short-term hype. At the exhibition, it’s crucial to understand whether the region’s real estate demand is primarily driven by long-term local residence or relies more on external investment or short-term behavior. The more genuine and stable the demand, the…

20/12/2025

20/12/2025

For many attendees, the initial motivation for participating in overseas real estate exhibitions is often to gain a concentrated understanding of investment opportunities in multiple countries and regions within a short period. However, in the information-dense and project-rich exhibition environment, focusing solely on property prices, promotional slogans, or short-term return expectations can easily lead to being attracted by appearances and overlooking the core factors that truly determine the success or failure of real estate investment. Against the backdrop of a constantly changing global economic environment, the logic of real estate investment is shifting from “where to buy” to “why buy.” This is especially true for overseas real estate, which involves deeper issues such as institutional differences, long-term development directions, and the suitability for individual planning. The 2026 Wise Shanghai Overseas Real Estate, Immigration, and Study Abroad Exhibition (March 29-31, 2026) brings together real estate, immigration, and education information from multiple countries and cities, providing attendees with a platform for systematic comparison and rational judgment. Is the Country and Region Stable? At exhibitions, one often sees frequently mentioned “hot countries” or “emerging regions.” However, the first step in judging the prospects of real estate investment is not to follow the hype, but to return to the long-term stability of the country and region itself. At exhibitions, visitors should focus on: the maturity of the country or region’s system; the continuity of its policies; and the clarity and transparency of its real estate regulations. A stable market with predictable rules is often more suitable as a long-term investment target than a market with short-term flashes but high uncertainty. Judging Real Demand from Population Trends The core value of real estate comes from genuine housing demand, not marketing stories. When introducing projects at exhibitions, concepts such as “development potential” and “future plans”…

20/12/2025

20/12/2025

With the increasing demand for global asset allocation, overseas property investment has become a focus for many investors. However, determining the optimal time to invest overseas requires a comprehensive consideration of factors such as policy, market conditions, and the economy to make an informed decision. The policy environment is a crucial variable influencing the timing of overseas property investment. Different countries and regions have constantly evolving policies regarding foreign investment in real estate. For example, some regions have implemented policies restricting the purchase of real estate by companies and individuals from specific countries, directly impacting the supply and demand dynamics of the local overseas property market. Conversely, some regions have introduced residency programs through real estate investment to attract foreign investment. For instance, some European countries offer residency status based on a certain amount of real estate investment. Such policy incentives often attract a large influx of investors, and seizing these opportunities can not only achieve asset allocation but also provide residency advantages. Investors need to closely monitor policy trends in their target regions and act decisively when policies are relaxed and foreign investment is encouraged. Market cycles are equally critical. The real estate market is cyclical, including boom, recession, depression, and recovery phases. During boom phases, prices rise continuously, and market transactions are active, but entering the market at this time may involve higher purchase costs and intense competition. During recessions or depressions, housing prices correct, and market supply becomes relatively excessive, reducing the cost of purchasing a home. However, it’s crucial to carefully assess the downside risks and determine if the market has bottomed out. For example, in one region, after experiencing market overheating, a period of adjustment led to a significant drop in housing prices. At this time, some investors with a long-term perspective began to position…

19/12/2025

19/12/2025

Driven by globalization, overseas property investment has become a crucial asset allocation option for high-net-worth individuals. However, significant differences exist in legal systems, property rights structures, and tax rules across countries. Ignoring compliance risks can lead to property disputes, heavy tax penalties, and even investment failure. This article analyzes the core legal aspects of overseas property investment from four dimensions: property type, legal procedures, tax compliance, and capital security, providing investors with a systematic guide. Property type is the primary consideration for overseas property investment. Most countries implement a freehold system, allowing investors to permanently own the land and buildings. Detached houses in countries like Australia and Portugal often fall into this category. However, some countries use a leasehold model, where land ownership belongs to the state or a specific institution, and investors only possess land use rights for a certain period. For example, some properties in Singapore have land leases of up to 99 years. Furthermore, apartment properties often involve shared ownership issues. Buyers only own their private area, while common areas such as corridors and elevators are shared by all owners. Any alterations to the appearance or use require the consent of more than two-thirds of the owners’ meeting. Such differences in property rights directly impact a property’s appreciation potential and inheritance prospects. Investors must verify the property’s nature with official land registry departments or professional lawyers before purchasing to avoid asset devaluation due to title defects. Compliance of legal procedures is crucial for transaction security. Property purchase procedures vary significantly from country to country, with some countries mandating lawyer involvement in title searches and contract review. For example, in Canada, lawyers must conduct title searches to confirm the absence of mortgages, disputes, or unpaid taxes; Thailand requires foreigners purchasing apartments to apply for foreign investment quotas through…

19/12/2025

19/12/2025

In the European immigration landscape, the Greek real estate investment immigration program continues to hold a popular position due to its “low investment, high returns” characteristics. Since the introduction of the “€250,000 real estate investment for residency” policy in 2013, the program has attracted tens of thousands of families worldwide to achieve residency through real estate investment. Despite several policy adjustments in recent years, its core advantages remain solid, making it a preferred option for middle-class families planning overseas residency, asset allocation, and children’s education. The stability of the policy framework is the core attraction of the Greek real estate investment immigration program. Under current law, non-EU citizens only need to purchase real estate worth €250,000 or more to apply for permanent residency for their entire family. This threshold is relatively low among European investment immigration programs, and there are no requirements for language, education, business background, or proof of funds. It is worth noting that after the policy adjustment in 2024, the investment threshold for some popular areas (such as tourist islands and core business districts) will increase to €500,000 to €800,000, but the classic €250,000 route can still be retained through “commercial-to-residential conversion” projects. These projects allow investors to convert commercial or industrial buildings into residential properties, with no restrictions on location, providing a flexible solution for families with limited budgets. The deep link between residency and real estate is another key feature of this policy. Applicants must hold onto real estate long-term to maintain their residency; selling the property immediately invalidates the residency status for the entire family. While this rule restricts asset liquidity, it also ensures policy continuity—as long as the property is held, residency continues. For investors, choosing a property requires considering both residential needs and appreciation potential. Data shows that properties in Athens’ city…

18/12/2025

18/12/2025

With the continued rise in global investment, more and more individuals and families are turning their attention to overseas real estate markets. For most investors, purchasing property is not only a means of preserving and increasing wealth, but also an important way to upgrade their lifestyle and allocate global resources. However, overseas property purchases typically involve significant capital investment, making loans a crucial option for many investors. Compared to domestic mortgage loans, overseas mortgage loans have more complex rules and conditions, involving factors such as the financial systems, legal regulations, and foreign exchange controls of different countries. Loan Feasibility Whether an overseas property purchase can be financed depends on the financial policies and banking regulations of the country where the property is located. Most countries allow non-residents to apply for housing loans, but loan amounts, interest rates, and repayment periods may differ from those for local residents. Generally, international or local banks set higher down payment ratios for overseas buyers to reduce loan risk. Meanwhile, some popular investment cities may have strict restrictions on foreign buyers, even requiring specific residency status or additional guarantees. Therefore, before planning to purchase a property with a loan, investors need to fully understand the policy environment of the target country to determine loan feasibility and available conditions. Loan Application Requirements Overseas property purchase loans typically require applicants to meet certain eligibility criteria. First, creditworthiness is a core factor in bank loan approval. A good personal credit history and stable income increase the likelihood of loan approval. Second, lending banks usually require applicants to provide detailed financial information, including income statements, tax returns, and bank statements, to assess repayment ability. Furthermore, loan applicants may need to make a relatively high down payment, typically between 30% and 50%, to reduce bank risk. Some countries may…

Number

NumberCall Now:

139 1723 4508

WeChat

WeChat

Form

FormBook Your Booth

Complete your information immediately and provide you with exclusive services!

Back to Top