-

Whatsapp

+1 689 248 1956 -

Email

joannewong0817@gmail.com

03/04/2026

03/04/2026

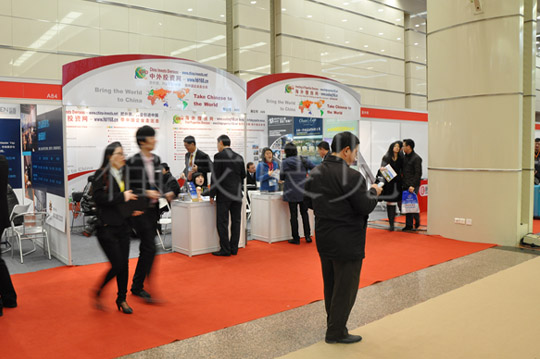

When considering attending overseas property exhibitions, many people weigh the time investment against the actual gains. With numerous information channels available, the continued value of offline exhibitions becomes a question worth considering. Overseas property exhibitions, by showcasing projects from multiple countries and providing opportunities for face-to-face interaction, allow attendees to access richer content within a limited time. This format helps to quickly build an overall understanding and makes comparison and selection more intuitive. Centralized Information Improves Time Efficiency A unified platform makes information acquisition more efficient. Exhibitions bring together property projects from multiple countries and regions, allowing attendees to browse a variety of options in a short time. Reduces Time Waste from Repeated Searches: Comprehensive information can be obtained without repeatedly searching across different channels. This centralized approach makes the time investment more valuable. On-site Interaction Enhances Judgment Speed Communication makes information understanding more direct. By communicating with project owners or consultants, key points can be quickly grasped, reducing misunderstandings. The Q&A process also speeds up the selection process: Obtaining answers tailored to individual needs helps to quickly identify areas of interest. This interaction makes decision-making more efficient. Multi-project comparison improves selection quality The same setting facilitates horizontal comparison. Different projects are presented simultaneously on-site, allowing visitors to directly compare their features and advantages. The comparison process also helps optimize choices: by analyzing differences, unsuitable options can be eliminated more quickly. This approach makes time investment more worthwhile. In the environment of overseas property exhibitions, time investment often translates into clearer information and more efficient judgment. Visitors can gain a concentrated understanding of multiple projects and gradually clarify their direction through communication and comparison. This experience helps reduce impulsive decision-making and makes subsequent actions more targeted. Furthermore, repeated participation allows for continuous refinement of judgment…

02/04/2026

02/04/2026

When faced with real estate investment choices, many people hesitate due to information asymmetry or unclear judgment. This is especially true when dealing with overseas markets, where differences in policies, prices, and environments across regions can easily lead to uncertainty. Real estate exhibitions, by showcasing projects in a concentrated manner and providing opportunities for on-site interaction, allow investors to access information from multiple sources in a single space. Looking at the formats of overseas real estate exhibitions presented on relevant platforms, this scenario demonstrates its ability to foster intuitive understanding. Through comparison of multiple projects and communication, initially vague judgments gradually become clearer, thereby boosting investment confidence to some extent. Concentrated Display Makes Information More Transparent and Intuitive Presenting multiple projects simultaneously helps reduce cognitive biases. Exhibitions bring together real estate projects from different countries and regions, allowing investors to directly understand prices, locations, and basic information. Intuitive information also makes it easier to form a basis for judgment: On-site observation and data acquisition reduce reliance on a single source of information. This transparency helps enhance trust. Face-to-Face Communication Enhances Understanding Depth Communication moves information beyond the surface. Investors can directly communicate with project owners or consultants to learn more details and background information. Interactive processes can also resolve doubts: Asking questions about issues of personal concern helps alleviate concerns. This in-depth understanding helps strengthen confidence in judgment. Multiple comparisons aid in rational decision-making The comparison process makes advantages and disadvantages clearer. Comparing different projects in the same environment allows for the rapid identification of differences and characteristics. The analytical process also clarifies thinking: considering price, location, and development potential helps in selecting more suitable options. This rational analysis enhances decision-making confidence. In the environment of real estate exhibitions, information acquisition and communication are more direct, allowing…

27/03/2026

27/03/2026

When faced with numerous overseas property projects, efficient filtering is a major concern for many investors. Relying solely on online resources or fragmented channels often leads to overwhelming information and difficulties in comparison. Overseas property exhibitions, by showcasing projects from different countries and types in a unified space, allow visitors to quickly access key information. Through on-site demonstrations and communication, the filtering process eliminates the need for repeated research, enabling initial judgments to be made quickly. This approach not only improves efficiency but also provides a more focused selection process, laying the foundation for further in-depth understanding. Centralized Display Makes the Filtering Path Clearer A unified setting reduces interference from scattered information. Multiple countries and projects presented at the same exhibition allow visitors to quickly browse different property types and price ranges. Comparing multiple projects in the same environment helps to quickly eliminate options that do not meet requirements. This method makes filtering more efficient and organized. On-site Communication Helps Identify Key Projects The interaction session makes judgments more accurate. By communicating with staff, you can quickly understand the core information of a project, such as location, purpose, and basic conditions. Asking questions can speed up the screening process: Asking questions tailored to individual needs helps narrow down the choices quickly. This interactive approach makes the screening process more relevant to actual needs. Multi-dimensional information supports rapid decision-making It not only focuses on the property itself but also involves multiple aspects. Exhibitions often include information on market conditions and policy background, providing more references for screening. Comprehensive information helps improve judgment efficiency: Combining different factors allows for a faster determination of priority projects. Multi-faceted support makes the screening process more complete. Through overseas property exhibitions, investors can access a large amount of project information in a short…

27/03/2026

27/03/2026

Many people attending various exhibitions when considering overseas property investment often wonder: do each event introduce new projects? Compared to a one-time visit, continuous attention allows investors to observe market changes more comprehensively. Overseas property exhibitions typically bring together project resources from multiple countries and regions, and their content is often updated based on market dynamics at different times. This allows attendees to see changes in existing projects and access new properties and investment opportunities, providing a more comprehensive understanding and more reference points for decision-making. Market Changes Drive the Emergence of New Projects The market environment at different stages affects the pace of project updates. The real estate market is influenced by factors such as policy and demand, and new projects are gradually launched along with the development cycle. Exhibition organizers introduce new properties based on market conditions, keeping the exhibits updated. Therefore, each visit offers the opportunity to access different information. Changes in Exhibitors Lead to Content Differences Changes in participants affect the exhibition presentation. Different organizations exhibiting at different times may bring their own new projects or key promotional content. The focus of the exhibition will also vary: even the same organization may adjust its project portfolio according to different stages, offering visitors new options. This fluidity allows for variation in the exhibition content. Project updates and continuations coexist Not all content will be completely replaced. Some mature projects may continue to be showcased, facilitating long-term observation and comparison by visitors. The combination of old and new makes the information more complete. This approach allows visitors to both observe changes and make continuous judgments. Overseas property exhibitions typically introduce new projects while retaining some stable resources, creating a balance between updates and continuations. Through repeated participation, investors can gradually accumulate information and develop…

24/03/2026

24/03/2026

In today’s diversified investment environment, more and more people are paying attention to the rationality of asset allocation, especially turning their attention to overseas real estate markets. Faced with policy differences, market cycles, and investment thresholds across different countries, information obtained from a single channel is often insufficient for comprehensive judgment. Exposure to information from different markets in the same setting helps broaden horizons and provides more directions for asset allocation, making investment decisions more aligned with actual needs. Multi-country property showcases offer more choices for allocation This centralized presentation makes the characteristics of different markets clearer. Exhibitions typically bring together real estate projects from multiple countries and regions, allowing investors to quickly understand the price ranges and development potential of different markets. Diverse choices also make allocation strategies more flexible:Differences in property types and policies across different countries provide a basis for diversifying funds, helping to build a more balanced asset structure. Through comparisons across multiple countries, asset allocation is no longer limited to a single region. On-site communication helps understand investment logic Face-to-face communication makes information acquisition more concrete. Exhibiting organizations or consultants will introduce project backgrounds, market trends, and other content, helping investors understand the value logic of different properties. In-depth communication can also reduce information bias:Asking questions allows for a deeper understanding of details, such as holding costs and transaction processes, leading to more rational judgments. This interactive process makes allocation decisions more evidence-based. Multi-dimensional information integration enhances decision-making references Exhibitions focus not only on the property itself but also on related supporting information. This includes the local living environment, rental market, and policy conditions, providing investors with a more comprehensive reference dimension. Information integration makes planning more forward-looking. Combining real estate investment with long-term asset planning helps to form a clearer…

20/03/2026

20/03/2026

In the context of increasingly fierce competition in the real estate industry, a single customer acquisition method is no longer sufficient for long-term development. Offline exhibitions, as a highly concentrated resource-matching platform, are regaining importance. Regarding the question, “Can real estate exhibitions expand channels?”, the core value of international real estate exhibition platforms like OPI lies not only in project display but also in establishing connections between developers, distributors, and end customers. Through on-site communication and resource integration, exhibitions often create a more direct and trust-based cooperative environment than online platforms, making them a crucial method for many companies to expand their channels. Is Concentrated Acquisition of Diverse Channel Resources More Efficient? Real estate exhibitions bring together a large number of intermediaries, investment advisors, and partners, allowing companies to access different types of channel resources in a short period. Face-to-face communication makes it easier to screen for high-quality partners, reducing intermediate screening costs and improving channel expansion efficiency. Is Brand Exposure and Trust Building More Direct? At offline exhibitions, companies can enhance brand visibility and deepen the impression on potential customers through booth displays and project presentations. Real-world interactions foster trust more easily, laying the foundation for future cooperation or transactions. Is the customer acquisition path more precise? Exhibitors typically have clear investment or home-buying intentions, allowing companies to directly reach their target customer groups. On-site consultations and communication enable quick assessment of customer needs, thereby optimizing product recommendations and sales strategies. Is the industry resource integration capability improved? Exhibitions are not only sales channels but also information exchange platforms, providing insights into market trends and competitive dynamics. Establishing connections with upstream and downstream resources helps companies expand into broader cooperation models and achieve diversified channel layouts. Real estate exhibitions act as “resource amplifiers,” efficiently…

19/03/2026

19/03/2026

In an environment of ever-intensifying industry competition, real estate exhibitions serve as highly concentrated hubs for exchange, offering companies multifaceted opportunities to showcase their strengths, expand their channels, and gather vital information. Participation in these exhibitions not only allows a wider audience of potential clients and partners to become acquainted with the company, but also facilitates the rapid establishment of an extensive professional network within a short timeframe. Transforming the inherent value of this platform into tangible results is a key priority for many enterprises. Through systematic participation and strategic optimization, real estate exhibitions can play a constructive role in brand communication, resource integration, and business expansion—thereby providing a more solid foundation for corporate growth. Expand Brand Exposure and Enhance Market Awareness Real estate exhibitions provide companies with a centralized platform for showcasing their offerings. On-site displays reinforce visual impact:Through strategic booth design and content presentation, brands become more distinctive and recognizable. Increase industry visibility:Attract the attention of potential clients, partners, and stakeholders. The continuous accumulation of exposure helps companies establish a clearer and more defined position within the market. Facilitate Precise Matching of Clients and Projects The exhibition environment fosters efficient communication and rapid screening. Face-to-face interaction boosts efficiency:Direct dialogue makes it easier to understand specific needs and intentions. Shorten decision-making cycles:Information transparency helps accelerate the pace of potential collaborations. Precise matching ensures a more efficient and effective utilization of resources. Expand Cooperation Channels and Broaden Growth Horizons The participation of diverse stakeholders transforms exhibitions into hubs for resource convergence. Connect with various partner types:Including investors, channel distributors, and service providers. Forge diverse collaborative relationships:Opening up a wider array of growth possibilities for the company. The expansion of cooperation channels provides a sustained source of momentum for corporate development. Gather Industry Intelligence and Optimize Growth Strategies…

18/03/2026

18/03/2026

在全球市场一体化程度日益加深的背景下,企业间的合作方式日趋多元化和开放。海外房地产展会正日益受到重视,它不仅是项目展示的平台,也为不同利益相关方提供了便捷的对接渠道。通过汇聚优质资源、促进面对面交流,参展商能够更直接地了解彼此的需求,从而推动合作。与传统渠道相比,这种高效的对接方式更具针对性,也更有可能取得切实成果。 资源集中使合作更容易 海外房地产展会整合分散资源,使合作机会更加清晰可见。 多方利益相关者沟通:开发商、分销商和投资者可以在同一空间进行沟通,减少中间商造成的信息损失。 提高合作匹配效率:现场沟通可以快速识别合适的合作伙伴。 资源的集中呈现将合作从搜索转变为选择,使过程更加高效。 面对面交流增强合作潜力 直接沟通在商业合作中具有无可替代的优势,有助于建立关系。 更直观、更深入的沟通:现场交流可以及时解答问题,明确合作意向。 更短的决策周期:减少重复沟通所花费的时间,有助于更顺畅的合作。 这种高效的互动使得将合作机会转化为具体行动变得更加容易。 信息透明度增强合作信心 充足的信息是合作的关键前提,而展览会可以提供更全面的参考资料。 更清晰的项目和市场信息:参展商可以获取各种信息,从而更全面地了解情况。 降低合作中的不确定性:信息透明度有助于降低风险担忧,提高合作意愿。 信息清晰,合作中更容易达成共识。 品牌展示巩固合作基础 展现企业形象和实力对建立合作关系具有重要影响。 提升企业信誉:展现自身优势能让合作伙伴更容易建立信任。 增强品牌知名度:持续曝光可以加深印象,并为合作创造条件。 良好的品牌展示能够为商业合作提供稳定的支持。 多元化机遇拓展合作空间 展览会将不同背景的参与者聚集在一起,创造更多合作的可能性。 联系更多潜在合作伙伴:在短时间内建立广泛的联系并拓展合作渠道。 探索新的合作方向:交流可以发现更多潜在的合作模式。 多元化的机会使商业合作更加灵活和可扩展。 海外房地产展会具有资源整合、信息交流和沟通效率方面的显著优势,能够有效促进企业合作。在这样的环境下,企业可以更快地建立联系,更深入地了解潜在合作伙伴,从而减少不必要的试错过程。通过持续参与和经验积累,合作关系能够逐步从短期联系转向长期发展。同时,展会提供的多元化机遇也为企业选择合作路径提供了更大的灵活性。在当今跨境合作日益频繁的背景下,这一高效平台的价值将持续凸显,为企业合作提供更加稳定灵活的支持。

17/03/2026

17/03/2026

Against the backdrop of increasingly frequent cross-border investment and global resource flows, cooperation models in the real estate industry are constantly expanding. Overseas real estate exhibitions are gradually becoming an important window for enterprises to explore international markets. They not only serve as project showcases but also build efficient communication bridges for various stakeholders. On such platforms, developers, distributors, and investors from different countries and regions can directly exchange ideas and quickly establish connections. Compared to traditional methods, this centralized form of communication is more efficient and facilitates actual cooperation. By continuously optimizing the display and matchmaking mechanisms, exhibitions are becoming an important vehicle for promoting business cooperation, allowing enterprises to find development opportunities in a broader market environment and making cooperation paths clearer. Centralized Resource Matching Facilitates Cooperation Overseas real estate exhibitions provide a concentrated opportunity for various resources to be showcased, making cooperation easier to achieve. Multi-type Resources Converge: Developers, agencies, and investors appear on the same platform, reducing the time cost of finding partners. Efficient Communication Speeds Up Cooperation: Face-to-face communication can quickly clarify needs and cooperation directions, helping to advance the cooperation process. Through the centralized integration of resources, the process from initial contact to final implementation of cooperation is effectively shortened. Increased Project Exposure Drives Business Opportunities Exhibitions provide projects with broader display channels, allowing more potential partners to learn about relevant information. Expanding Project Influence: On-site displays and promotions can garner more attention and recognition for projects. Attracting Diverse Partners: The participation of different types of visitors creates more cooperation possibilities for projects. Increased project exposure leads to more business cooperation opportunities. Strengthening Trust and Facilitating Cooperation Implementation Business cooperation relies on trust, and exhibitions have a unique advantage in this regard. Authentic Displays Enhance Credibility: On-site displays allow partners to…

17/03/2026

17/03/2026

In the context of continuous globalization, cooperation in the real estate industry is no longer limited to a single region. More and more companies are focusing on overseas markets, hoping to find cooperation opportunities through broader platforms. Overseas real estate exhibitions play a vital role in meeting this demand. They are not only windows for project display but also important bridges connecting resources from different countries. By showcasing various high-quality real estate projects and services in a concentrated manner, participating parties can achieve efficient communication in the same space, thereby promoting the establishment of cooperative relationships. For companies, these exhibitions not only help expand markets but also provide opportunities to acquire more industry information through exchanges, making their development direction clearer. Concentrated Resource Display Improves Matchmaking Efficiency Overseas real estate exhibitions bring together projects and companies from different regions, providing a good foundation for cooperation. Multiple Resources Presented on One Platform: Developers, investors, and service providers can exchange information in the same setting, reducing the time cost of information acquisition. Face-to-Face Communication is More Efficient: On-site exchanges can quickly build trust and are more conducive to a deeper understanding of cooperation needs. By concentrating resources, cooperation opportunities become clearer, and communication becomes smoother. Facilitating Cross-Regional Information Exchange Information sharing is crucial for international cooperation, and exhibitions serve as an important channel for achieving this. Understanding Different Market Characteristics: Exhibitors can obtain relevant information on market environments and project situations in various regions through exchanges. Enhancing Decision-Making Value: Abundant information sources help in making more comprehensive judgments before cooperation. Strengthening information exchange makes cooperation more rational and feasible. Strengthening Brand Trust and Cooperation Foundation Trust is an important prerequisite in international cooperation, and exhibitions can strengthen this to a certain extent. Showcasing Corporate Strength and Project Advantages:…

14/03/2026

14/03/2026

As global real estate markets continue to develop, more investors are paying attention to overseas property investment. Compared with concentrating assets in a single region, overseas real estate can help diversify investment risks while offering potential rental income and long-term asset appreciation. However, because cross-border property investment involves legal systems, transaction procedures, and financial arrangements in different countries, it usually follows a structured process. Understanding the overall investment procedure in advance can help investors plan each step more clearly and reduce uncertainties during the process. Many investors also attend real estate exhibitions or investment expos to learn about international property projects and investment procedures before making decisions. Market research and project selection before investing Before entering an overseas real estate market, investors need to conduct thorough research and carefully select potential projects. The main goal of this stage is to understand the real estate environment of the target country and determine the most suitable investment direction. Define investment goals: Investors should clarify whether the purpose is asset diversification, rental income, long-term appreciation, or future personal use, as this will influence the type and location of the property. Study national and city markets: Understanding the economic conditions, population movement, and property market trends of the target country helps evaluate long-term investment potential. Evaluate specific real estate projects: Consider factors such as property location, transportation access, surrounding facilities, and future development plans. Review the developer’s background: Investigate the developer’s reputation and past projects to ensure the quality and reliability of the development. At this stage, investors often review market reports, consult professional advisors, or attend real estate exhibitions to compare property opportunities across different countries. Property transaction procedures and legal verification After selecting a suitable property project, investors move into the formal transaction stage. Because legal systems differ from country to…

12/03/2026

As global economic connections continue to strengthen, more investors are paying attention to overseas real estate markets. Compared with concentrating assets in a single region, overseas property can provide more diversified investment channels and may also generate rental income and long-term asset appreciation. With the acceleration of global capital flows, overseas real estate has gradually become an important option for many families when planning their assets. Many investors also attend real estate exhibitions or investment expos to learn about property markets and opportunities in different countries, helping them identify suitable investment directions. Growing demand for global asset allocation As wealth accumulation increases and awareness of international investment expands, more investors are beginning to allocate assets globally. Risk diversification: Investing in real estate across different countries can help reduce the impact of fluctuations in a single market. Long-term asset preservation: Some international property markets are relatively stable and can help investors maintain long-term asset value. Diversified investment channels: Overseas real estate provides an alternative investment option compared with stocks or financial products. Cross-border living needs: Some investors want to own property abroad for vacation, retirement, or their children’s education. Overseas real estate market potential attracts investors Different countries and cities are at different stages of development, and some emerging cities or popular regions offer significant growth potential. Urban development driving property value: Infrastructure improvements and economic growth can stimulate real estate markets. Stable rental demand: Many international cities have strong rental markets that can generate rental income for investors. Tourism and commercial development: Tourist destinations and major business centers often attract strong property demand. Increasing global mobility: The growing movement of people across countries also supports housing demand in international cities. Many investors learn about property projects from different countries during real estate exhibitions or investment expos, allowing them to…

Number

NumberCall Now:

139 1723 4508

WeChat

WeChat

Form

FormBook Your Booth

Complete your information immediately and provide you with exclusive services!

Back to Top